by Scott Denne

Both strategic acquirers and sponsors have increased their purchases of application software vendors as the market for those targets accelerates beyond last year’s record. As those buyers stayed active, the largest deals grew larger and multiples continued to climb. Rising valuations for growth companies in the public markets – both new offeringsand already-public businesses – have pushed up pricing for software targets and could help propel deal sizes through the rest of the year.

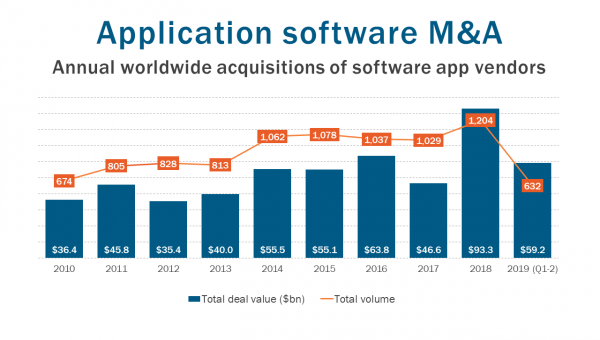

According to 451 Research’s M&A KnowledgeBase, 632 application software providers have been acquired for a combined value of $59.2bn, on pace to top last year’s record haul in both value and volume. In our analysis of last year’s activity (published as part of 451 Research’s Tech M&A Outlook 2019), we noted that 2018 marked the first year that acquisitions of application software vendors crossed 1,100 as both strategic buyers and private equity firms accelerated their purchases.

The same trend has driven this year’s market as well. Both categories of acquirers are up from last year’s pace. Yet the number of big-ticket transactions is down a bit. While 29 application software providers sold for $1bn or more in 2018, only nine have done so this year. But those that have crossed the 10-figure mark have done so in a big way. Since the bursting of the dot-com bubble, only four such targets have sold for more than $10bn and two of them (Tableau Software and Ultimate Software) did so this year.

To be clear, the relative decline in the number of big-ticket acquisitions hasn’t pulled down the total deal value. If the current pace of deal value were to hold through the end of the year, it would finish more than one-quarter higher than last year, which smashed the previous record by nearly 50%. Put another way, at the midpoint of 2019, the total value of application software transactions is higher than all but two full years, our data shows.

Although fewer software vendors have sold for north of $1bn, those that have are fetching higher prices. According to the M&A KnowledgeBase, the median multiple for those deals this year stands at 8.1x trailing revenue, nearly a full turn above last year’s total. That rise comes amid a 22% year-to-date increase in the Nasdaq index and a welcoming environment for new tech listings, including software companies like Slack and Zoom Video, which commanded 62x and 41x multiples at the midpoint of the year, following their recent public market debuts. Such a compelling alternative exit could continue to boost acquisition prices.