Contact: Scott Denne

A pair of private equity (PE) firms has taken CommerceHub off the public markets in a $1.1bn acquisition. The deal carries a scorching multiple that punctuates the value of e-commerce software as retailers struggle to make digital engagement a centerpiece of their business.

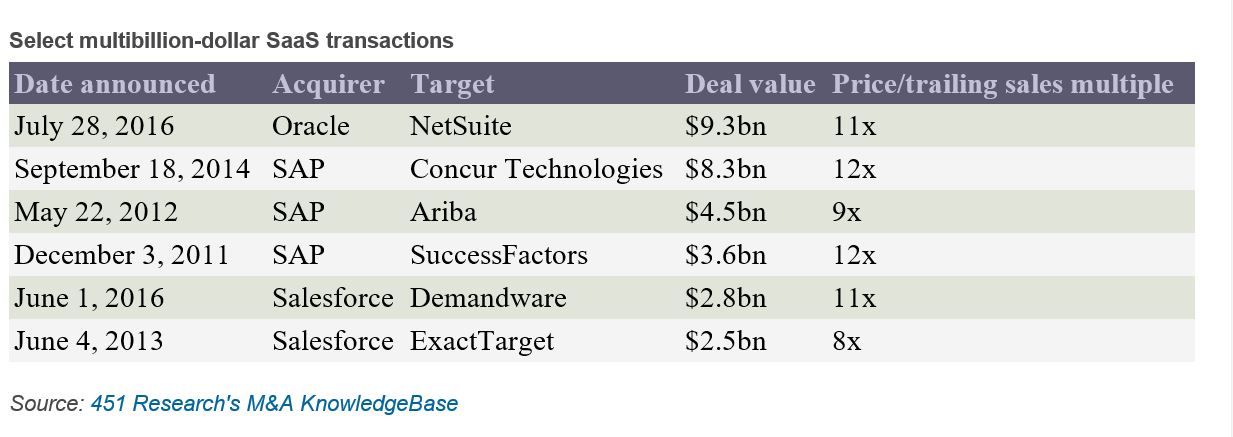

GTCR and Sycamore Partners’ joint purchase of CommerceHub values the firm at 10x trailing revenue, or 32x EBITDA – atypical multiples for an e-commerce software provider with the target’s growth. With that valuation, CommerceHub finds itself in the same neighborhood as Demandware and hybris, which each fetched about 11x revenue in their respective sales to Salesforce and SAP.

Yet CommerceHub’s revenue expanded by just 11% last year, compared with Demandware and hybris, which both posted topline growth in the 50% neighborhood leading up to their exits. Ariba offers a more accurate, if aging, comp for CommerceHub – both vendors provide back-end commerce services, such as integration between retailers and suppliers, whereas Demandware and hybris build customer-facing software. CommerceHub is fetching a multiple that’s a full turn above Ariba’s 2012 sale, despite the latter company having double the growth rate and being triple the size of the former.

In part, today’s multiple reflects higher prices being paid by buyout shops as their investments in tech M&A rise. According to 451 Research’s M&A KnowledgeBase, the median multiple paid by a PE acquirer last year rose to 3x, up from 2.5x a year earlier. Moreover, that median has hovered above 2.5x every year since 2014. In the preceding decade, it never once hit that level, and in only three years did the median reach 2x.

All that’s not to say nothing but a flood of PE money drove up CommerceHub’s price. Digital commerce technology is evolving into a core element of customer engagement and retailers need timely, accurate product information, which CommerceHub facilitates, to integrate into their customer-facing marketing and commerce software systems. According to 451 Research’s VoCUL Quarterly Advisory Report: Digital Transformation Leaders and Laggards, digital commerce and web experience management are the two most common areas of investment for enterprises, as 27% of enterprises told us they plan to deploy or upgrade those technologies in late 2017 and early 2018.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.