by Brenon Daly

Despite EU and UK leaders agreeing to terms on the country’s departure from the larger political and economic body, there’s still no actual Brexit. A weekend vote on the accord now looms large in the British Parliament, with early forecasts indicating the hard-won deal will likely struggle to get final approval. Parliament rejected a similar agreement earlier this year.

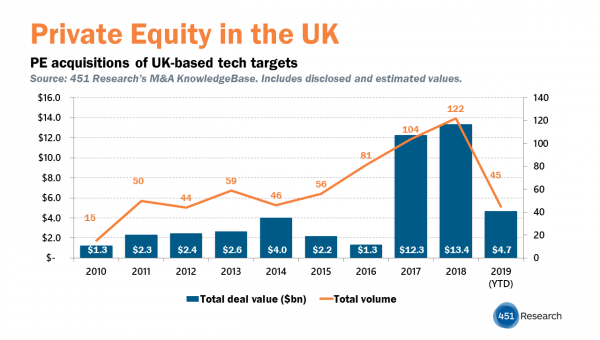

Regardless of whether the ‘ayes’ or the ‘nays’ carry the vote about the EU bloc, Brexit has already notably diminished the UK’s standing in another large marketplace: tech M&A. British buyers as well as British sellers in 2019 are on pace to announce their fewest tech deals in a half-decade, according to 451 Research‘s M&A KnowledgeBase. The slowdown there is being felt much more broadly, since our data shows the UK has perennially ranked as the second-busiest M&A market in the world.

Deal volume – both on the buy- and sell-side – is on track this year to drop about one-quarter from the recent highs they hit. Incidentally, our M&A KnowledgeBase indicates that tech M&A in the UK peaked in 2015 – the year before the Brexit vote. Since the contentious vote in mid-2016 and the still-unresolved results, the number of British tech prints has dropped every year.

Somewhat unexpectedly, however, recent M&A spending has clipped along at exceptional levels. Based on annualized totals for year-to-date activity from our M&A KnowledgeBase, British buyers will spend a record amount on tech acquisitions in 2019, while spending on acquired UK-based tech companies is on pace for its second-highest annual level.

For dealmakers, Brexit has essentially meant fewer bets but much bigger bets. As an example, consider this week’s take-private of British endpoint security vendor Sophos. To erase Sophos from its home on the London Stock Exchange, Thoma Bravo is paying $3.8bn. To put that price into context, the Sophos take-private is more than the combined price of the buyout firm’s two next-largest information security LBOs.

As the sale of Sophos also shows, deals can still be struck in times of uncertainty, but extra work is required. More than three years since the original decision, Brexit has left open vexingly large questions for businesses, such as taxation rates, employee permits and supply chains. All of those have a direct impact on a company’s valuation, which is the key consideration in all acquisitions. Fittingly enough for the contentious three-year Brexit process, the British Parliament’s vote this weekend may only add to the volatility.