by Scott Denne

Fintech deals keep coming as Morgan Stanley shells out $13bn of its stock for online financial broker E*TRADE. As we’ve previously noted, payments and financial services firms accounted for an outsized share of this year’s and last year’s deal activity as they look to acquisitions to align with changes to the tech landscape.

Morgan Stanley’s move isn’t driven so much by E*TRADE’s technology as much as it’s driven by access to the target’s retail clients. Over the past five years, Morgan Stanley has transformed its business through a focus on wealth management, particularly at the high end of that market. That business today accounts for just over half of its pretax profit, up from one-quarter five years ago. The E*TRADE buy extends that business into smaller retail investors – the seller manages an average of $70,000 per client, less than one-tenth of Morgan Stanley’s average client.

E*TRADE isn’t exactly a tech vendor, but it wouldn’t be able to service so many small clients without its online interface. And that’s illustrative of many of the recent fintech deals we’re seeing – it’s not that financial services providers are buying tech so much as they’re buying into markets that are opened by tech. While online brokerages, which have been around since the dot-com days, aren’t new, the growth of the category and the entry of startups have driven competition to new heights, causing most players to drop their fees and find buyers.

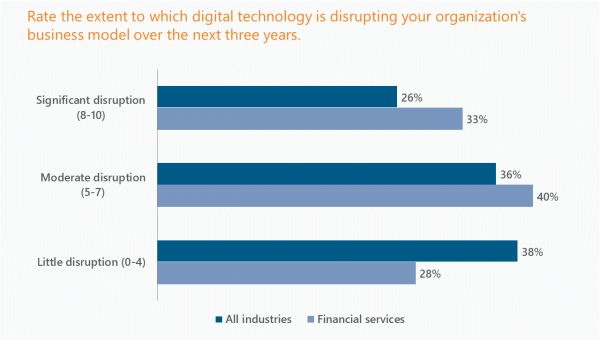

Banks aren’t the only companies in financial services printing major acquisitions to move into tech-enabled markets. For example, Visa, in its largest-ever tech deal, paid $5.3bn last month for Plaid, a maker of payment-processing APIs for software developers as more payments happen via e-commerce sites, mobile apps and other software interfaces. We’re likely to continue to see transactions along a similar vein as financial services firms broadly expect technology to impact their market. According to 451 Research‘s Voice of the Enterprise: Digital Pulse, Budgets & Outlook, one of every three employees of finance companies expect digital technologies to significantly disrupt their business model in the next three years, compared with just one in four across all industries.

Figure 1: Level of digital disruption expected in next three years