Contact: Brenon Daly

AT&T’s planned $48.5bn purchase of DirecTV has one thing going for it that Comcast’s similarly sized acquisition of Time Warner Cable doesn’t: customers don’t necessarily hate the providers. That’s at least one way to handicap the outlook for the two proposed pairings, which total, collectively, about $94bn in transaction value. The two deals represent the second- and third-largest tech transactions since 2003.

In the end, the return on both of these mammoth bets by telcos will be determined by how well the new owners serve customers. On that count, AT&T – both by itself and with the addition of DirecTV – has much more goodwill among TV consumers that Comcast-Time Warner Cable, according to ChangeWave Research, a service of 451 Research. In a March survey of 4,375 North American residents, about one-quarter of respondents said they are ‘very satisfied’ with AT&T U-verse and DirecTV. That was more than twice the level that said they are very satisfied with Comcast (11%), and four times the level for last-placed Time Warner Cable (a paltry 6%).

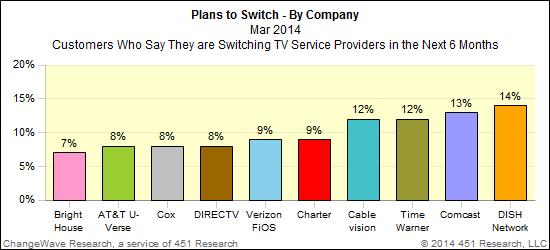

Perhaps more importantly, the ChangeWave survey indicates that TV subscribers aren’t planning to stick with the service they don’t like. (We would note that for service providers, which rely on monthly billing subscription fees to offset huge capital expenditures, churn is particularly corrosive to business models.)

According to ChangeWave, one in eight respondents said they plan to switch from either Comcast or Time Warner Cable in the next half-year – half again as many who planned to jump from either AT&T U-verse or DirecTV. And where are the dissatisfied TV subscribers likely to look to get their fix of The Real Housewives of Orange County or SportsCenter ? Well, it just so happens that DirecTV and ATT U-verse are the most likely replacement service providers, according to ChangeWave.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.