by Brenon Daly

With Medallia’s paperwork closing out tech IPO activity for the first half of 2019, it’s worth taking a look back at the new listings so far this year. 451 Research will have a full report next week on the unusual flow in the IPO market, but our quick take is that Wall Street got back to business (as it were) with tech IPOs, and that the focus has been on quality, not necessarily quantity.

Not a single B2B tech company went public in Q1, a rare quarterly shutout for startups in a segment that typically finds a warm welcome on Wall Street. The slow start to this year for enterprise tech IPOs left the total number of completed offerings at just six for the first half of 2019, down from 10 offerings in the first half of 2018.

To be clear, we are tallying only B2B tech vendors listing on the two major US exchanges, so our count excludes this year’s IPOs by Pinterest and Uber, for instance. We would note, however, that these consumer tech names, unlike their enterprise brethren, received a rather bearish reception on Wall Street. The high-profile offerings of both Lyft and Uber are currently underwater.

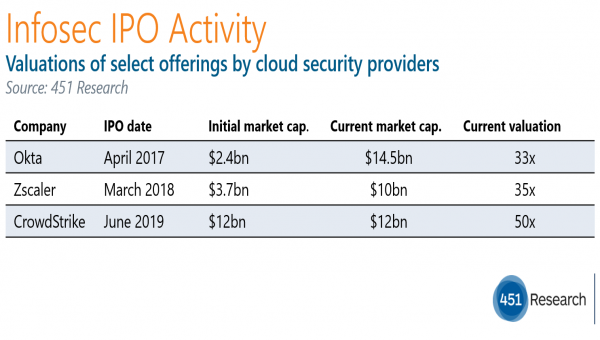

More significant than the number of enterprise tech startups coming public this year, however, is the stunning market value they are creating. Collectively, the six B2B companies that debuted in 2019 are valued at over $60bn, as of the end of Q2. For comparison, the 10 enterprise tech vendors that went public in the first half of 2018 created slightly more than $40bn of market value at the end of Q2 2018.

451 Research will have an in-depth report early next week on the stunningly rich valautions being awarded across the board to IPOs so far this year, as well as which startups from our coverage areas might be looking to cash in on Wall Street’s lucrative interest in enterprise tech right now.