by Brenon Daly

Even in a slump, it pays to be an information security (infosec) vendor. The latest company to realize the advantage of doing business in this red-hot market is Forescout Technologies, which is heading private in a $1.9bn deal with a pair of buyout shops. The network access control provider is set to exit Wall Street with a rather rich sendoff, given the mediocre numbers it has put up recently.

Despite a few brief slips, Forescout held itself together for most of last year. Through the first three quarters of 2019, shares soared some 45%. But all of those gains were wiped out overnight in early October as the company whiffed on its sales and losses widened.

According to S&P Capital IQ, revenue growth in 2019 was less than half the 30%+ rate it had been in recent years. Further, the tepid performance is expected to continue, with Capital IQ reporting that the consensus forecast calls for just 12% sales growth at Forescout in 2020.

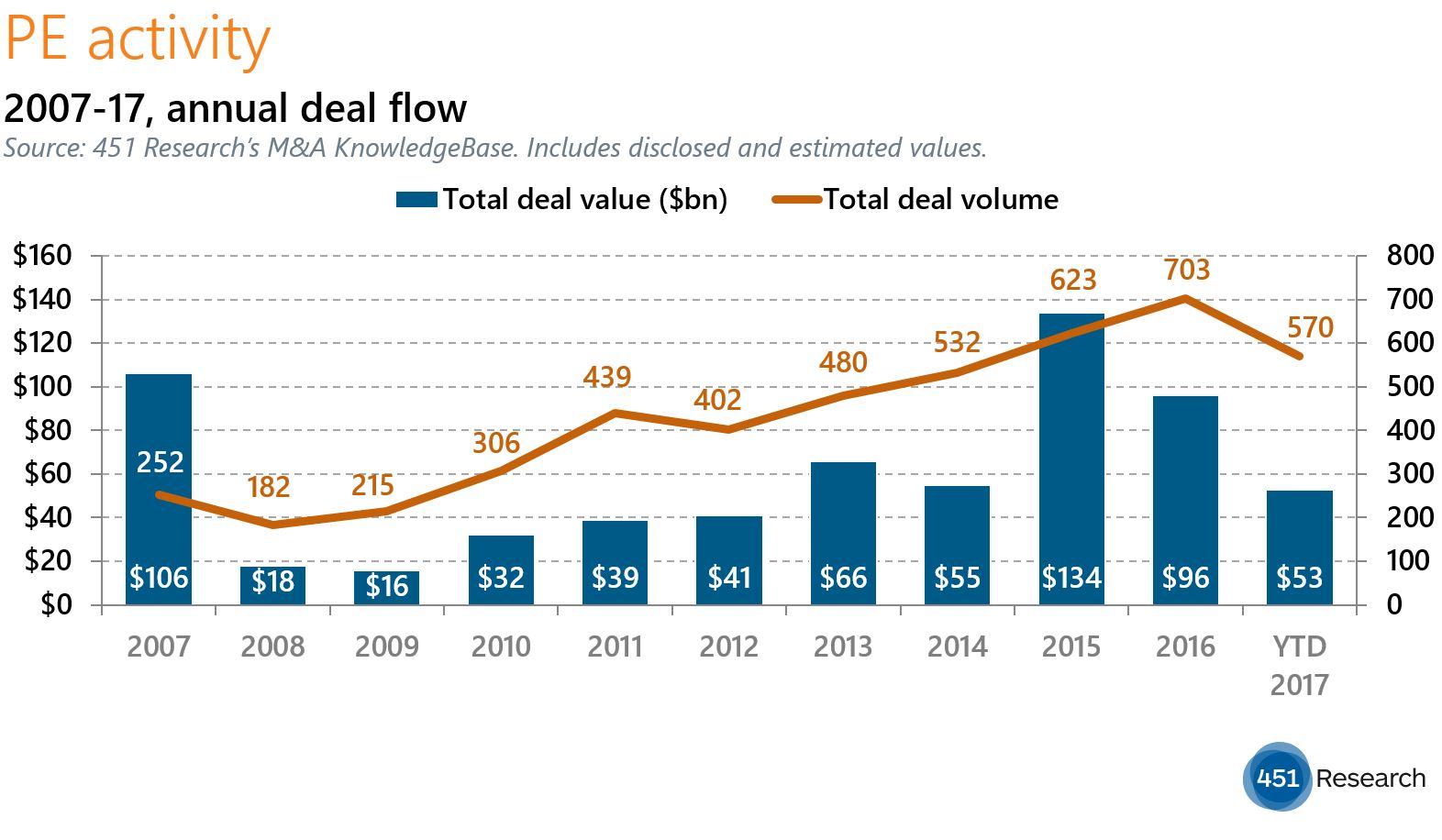

Yet the vendor’s slowdown barely shows up in the valuation being paid by Advent International and Crosspoint Capital Partners. By our math, the buyout duo is paying 5.5x trailing sales for Forescout. That’s significantly richer than the average valuation of 3.8x trailing sales for all take-privates recorded over the past year in 451 Research‘s M&A KnowledgeBase. Our numbers show that Forescout is valued fully two turns higher than both LogMeIn and Cision in their recent leveraged buyouts (LBOs).

Even in the infosec market – where premium valuations are the prevailing prices – Forescout’s looks heady. For comparison, the 5.5x trailing sales multiple for Forescout exactly matches the multiple paid in the industry’s most recent significant take-private, Thoma Bravo‘s $3.8bn LBO of Sophos last October.

That’s the same valuation, even though Sophos has a much more attractive financial model, particularly to cash-flow-focused operators. Sophos put up roughly the same growth rate as Forescout heading into their LBOs, but brings in almost twice as much revenue. Probably more important for the new private equity owners, Sophos throws off several hundred million dollars of cash flow each year, while Forescout is still burning cash.