Contact: Brenon Daly

Spending on tech deals in July hit its second-highest monthly total so far this year, driven by the widespread dealmaking of private equity (PE) firms. Buyout shops figured into eight of last month’s 10 largest acquisitions, either as a seller or a buyer. The big-dollar prints by financial acquirers in July continue the recent surge of unprecedented activity by PE firms, which have largely displaced corporate buyers as the ‘market makers’ for tech M&A.

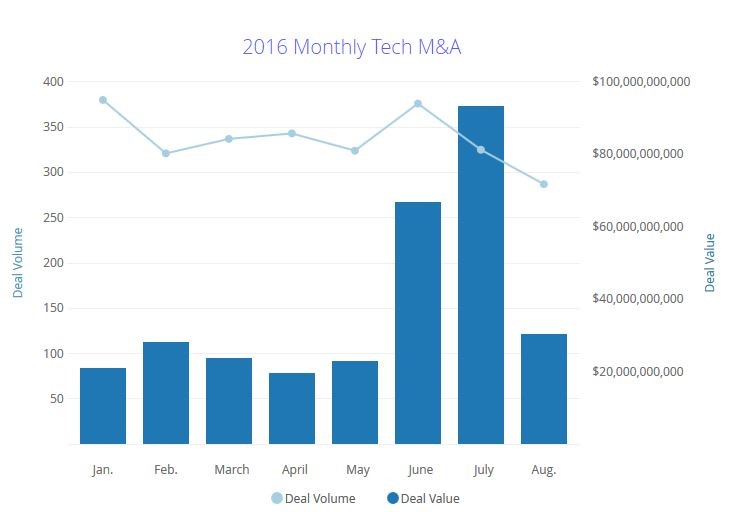

Overall, the value of tech transactions announced around the globe in July hit $28.9bn, roughly one-quarter more than the average month in the first half of the year, according to 451 Research’s M&A KnowledgeBase. Our research shows that PE firms accounted for some 40 cents of every dollar spent on tech deals last month — two to three times higher than the market share financial buyers held in recent years. Further, unlike the previous PE boom in the middle of the past decade that was dominated by single blockbuster transactions, the current record activity is coming from virtually all deal types.

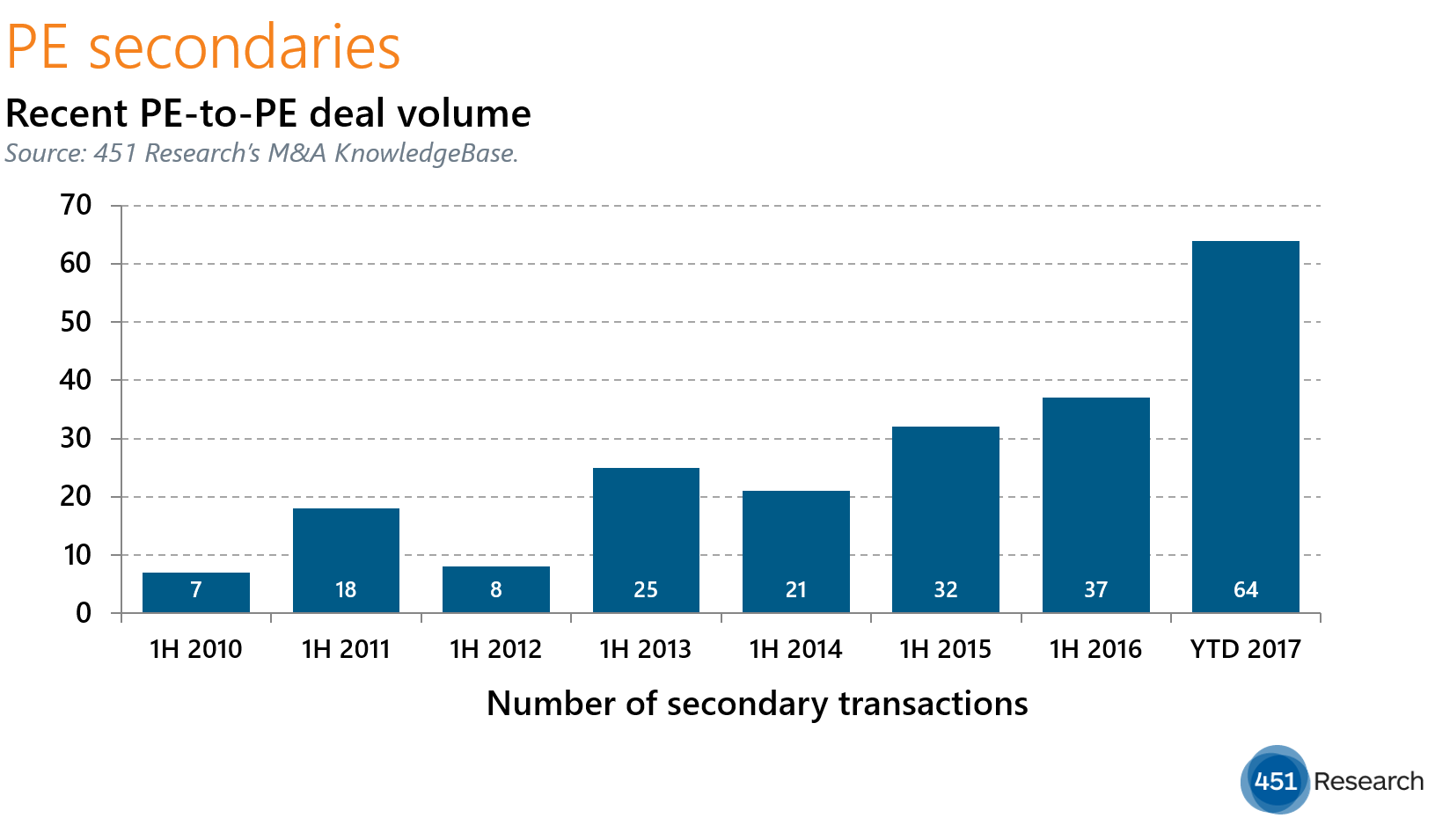

Just in July, we saw financial acquirers announce transactions ranging from multibillion-dollar take-privates (the KKR-backed purchase of WebMD) to ‘synergy-based’ midmarket consolidation (Francisco Partners’ Procera Networks won a bidding war with another buyout shop to land Sandvine) to early-stage technology tuck-ins (Vista Equity Partners’ TIBCO scooping up one-year-old nanoscale.io). Overall, according to the M&A KnowledgeBase, PE firms announced a staggering 77 deals last month. That brought the year-to-date total to 511 PE transactions in the first seven months of 2017 — setting this year on pace to smash the full-year record of 680 PE deals recorded last year.

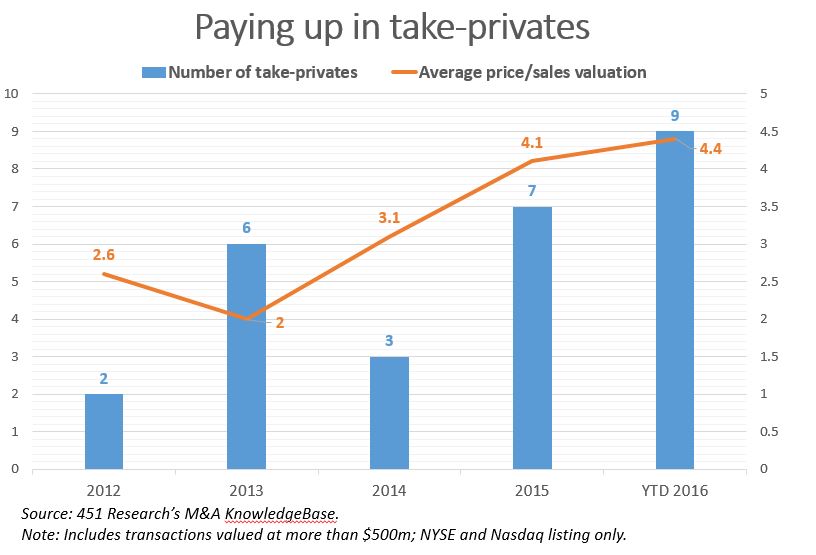

More broadly, last month featured a fair amount of old-line M&A, whether it was buyout firms trading companies among themselves (Syncsort) or mature tech industries consolidating (Mitel Networks reaching for ShoreTel or serial acquirer OpenText picking up Guidance Software, for instance). Those drivers put pressure on valuations paid at the top end of the market last month. According to the M&A KnowledgeBase, acquirers in July’s 15 largest deals paid just 2.4x trailing sales. Not one of last month’s 15 blockbusters got a double-digit valuation, although subscription-based ERP software startup Intacct came very close. For comparison, fully five of the 15 largest transactions in the first six months of 2017 went off at double-digit valuations.