by Brenon Daly

Tech M&A has started a bit sluggishly in 2020, but what about the rest of the year? Are tech buyers going to continue sitting on their hands, or will they be reaching for their checkbooks as the year moves along? And if they do go shopping, where will they be looking?

For answers to all of those questions and more, join 451 Research tomorrow (February 5) at 1:00pm EST for a special webinar, 2020 Tech M&A Outlook. (Register here.) During the hour-long webinar we will look at the broad-market trends shaping overall deal flow, as well as a special focus on two of the areas that we expect to see a surge in acquisition activity in the coming year:

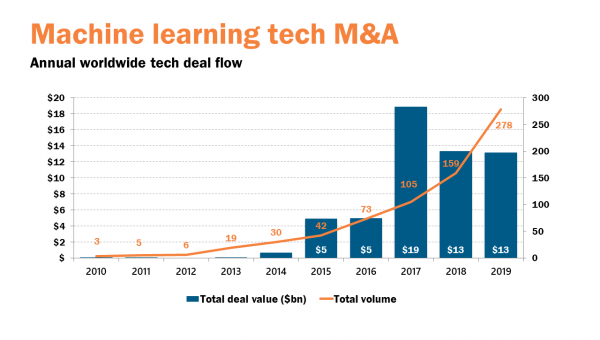

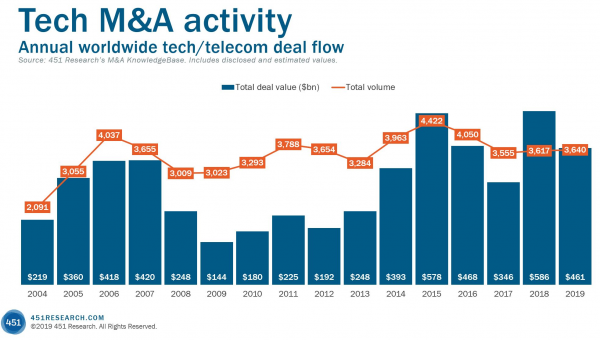

Over the past decade, machine learning (ML) has been the fastest-growing theme in all of tech M&A: 451‘s Research M&A KnowledgeBase shows that deal volume has been clipping higher at a CAGR of north of 50% over that period. As ML matures in the coming years, how will that affect acquisition activity?

Similarly, information security (infosec) has seen a dramatic uptick in dealmaking, with the annual number of prints in the sector running 50% higher in the back half of the past decade than during the opening half. That growth culminated in 2019 hitting a record for both the number and spending on infosec acquisitions. Where does the infosec M&A market go from here, and what sectors are going to see the most activity?

Again, tomorrow’s 2020 Tech M&A Outlook webinar will get you everything you need to know about what’s coming in the year ahead. We hope you can join 451 Research for our annual look at the multibillion-dollar tech M&A market.