Contact: Brenon Daly

As President Donald Trump approaches the end of his ceremonially important first 100 days in office, his approval rating has slumped to an unprecedented low. In fact, for the first time in modern politics, more people say they disapprove of Trump’s early moves as president than say they approve of them. However, there is one community that continues to support Trump, or at least say he’s been good for business: dealmakers.

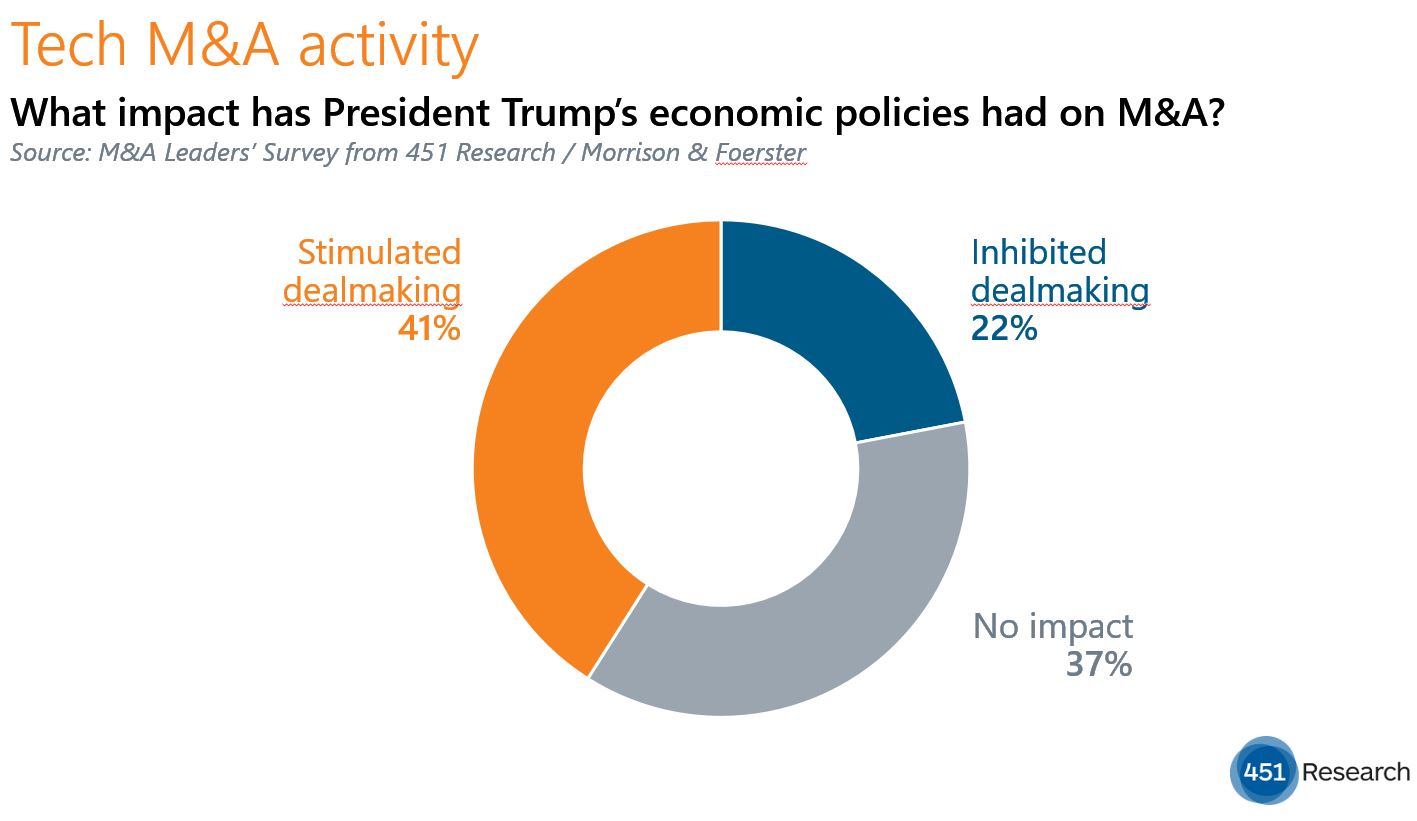

Four out of 10 (41%) respondents to the M&A Leaders’ Survey from 451 Research and Morrison & Foerster indicated that President Trump’s economic policies have stimulated dealmaking, almost twice the 22% that said his policies have slowed M&A. The results from the latest survey show a substantial reversal from our previous survey last October, which came amid an acrimonious battle with Hillary Clinton for the White House. At that time, nearly one-third (31%) said the election battle had slowed acquisition activity, compared with just 6% that said deals had sped up.

However, any boost that Trump and his policies might give to M&A won’t extend globally, according to the M&A Leaders’ Survey from 451 Research and Morrison & Foerster. Quite the opposite, in fact. Nearly half of respondents (47%) said Trump and his trade policies will slow cross-border acquisition activity, nearly twice the 26% that said the policies of President Trump – who campaigned on an ‘America First’ platform – will accelerate international dealmaking. We would highlight the fact that the bearish forecast for cross-border M&A is almost exactly the inverse of the positive influence Trump is expected to have on overall tech dealmaking, according to our survey respondents.