Contact: Brenon Daly

This time last year, the only sound coming from the tech IPO market was crickets chirping. Not a single company made it public in Q1 2016, the first quarterly shutout since the end of the recent recession. So far this year, there’s a lot more going on, even if the recent activity lags what we might have expected after a prolonged listless period for new listings.

What the current IPO market lacks in depth, however, it more than makes up for in variety. Just since 2017 opened, we’ve seen a number of ‘outlier’ events, including a multibillion-dollar dual-track exit, a unicorn rewarded on Wall Street, the largest consumer Internet offering in three years, and even a company use the circuitous route of a blank-check deal to go public. You know it’s a strange time for IPOs when a company that had been planning to go public on the Nasdaq but opted for a sale instead goes ahead and rings Nasdaq’s opening bell when that deal closes, as AppDynamics did.

There are other indicators of just how hard the tech IPO market is to read right now, including:

-AppDynamics scrapping its planned offering after Cisco swept in with a too-rich-to-pass-up $3.7bn offer in January, days before the software vendor was set to debut on Wall Street. As rich as AppDynamics’ sale was, however, the deal looked like a discount when fellow infrastructure software provider MuleSoft did hit the market almost two months later. MuleSoft’s trading valuation nearly matches AppDynamics’ terminal value, which included a premium.

-Both of the enterprise-focused tech firms that have gone public so far this year (MuleSoft and Alteryx) raised more money from private market investors than they did from Wall Street.

-And what to say about the IPO of Snap, which lost more money in 2016 than it took in as revenue? A five-year-old company that starts its prospectus by talking about ‘eyeballs,’ and then doesn’t give investors any say about how the business should be run in any case? A media company that went public just as it was experiencing its slowest audience growth? Despite all of those questionable metrics, Snap created more than twice the market value of all enterprise tech IPOs last year.

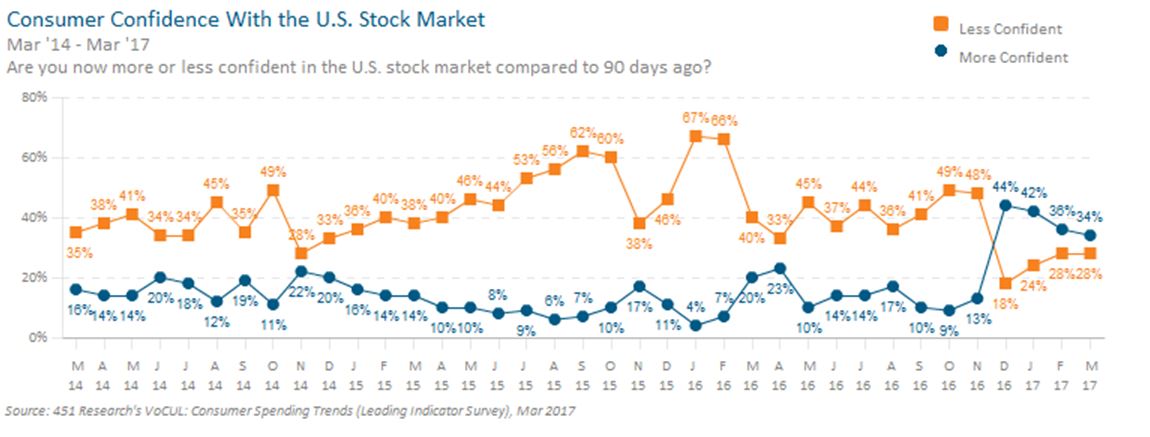

With Okta set to debut next week and several Hadoop vendors reportedly close to revealing their paperwork, the tech IPO market has enough to keep it going for the next few weeks. However, that doesn’t necessarily mean that Wall Street will be as welcoming as it has been. The US equity indexes are about 25% higher than they were during the bear market that mauled investors in the opening months of 2016. Yet all of the indexes have recently reversed, and are in the red for the past month. Meanwhile, 451 Research surveys of investors have shown a steady erosion of confidence in the stock market, which could give them pause before buying shares in any of the unknown and unproven tech startups looking to go public.