This year’s surging M&A market has brought relief to a tech sector that’s long struggled to find exits. With today’s announcement that Cisco is acquiring venture-backed Luxtera for $660m, venture capitalists have realized more value from their semiconductor investments than any time since 2013. In a reflection of the broader market, the return of strategic acquirers has boosted the sales of chip startups.

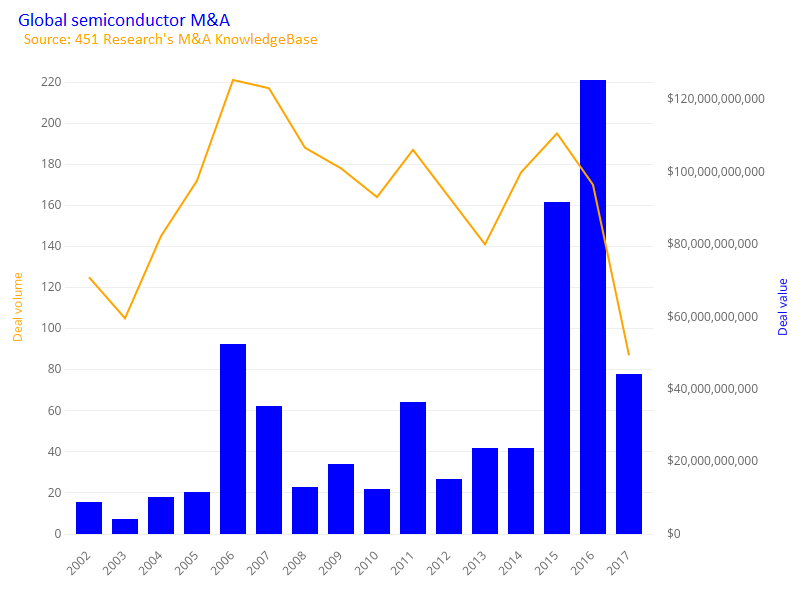

As 2018 heads toward a close, buyers have spent a collective $1.4bn on purchasing semiconductor startups from venture portfolios, compared with just $1.8bn in the three previous years combined. The acquisition of Luxtera goes a long way toward boosting this total. According to 451 Research’s M&A KnowledgeBase, the deal is the largest purchase of a VC-backed chipmaker since the dot-com bubble burst. (Neither that record nor the annual totals include acquisitions of public companies that previously raised venture capital.)

That Luxtera’s exit marks a record speaks as much to the dearth of liquidity for chip startups as it does to the target’s accomplishments. In the face of rising development costs, VCs have long shied away from chip investments and acquirers have come to depend on product development more than M&A for incremental improvements. Most of the dealmaking among semiconductor vendors in recent years has been large consolidations, rather than midmarket acquisitions.

Still, there’s been some relief from the paucity of exits this year. Prior to Luxtera, Cisco, a frequent buyer of software vendors in recent months, hadn’t acquired a semiconductor business in nearly three years. The same goes for Skyworks, which provided VCs with the third-largest exit in the category when it shelled out $405m for Avnera in August – it was the acquirer’s first purchase in more than 30 months. And Intel picked up a pair of chip startups this year after a 16-month hiatus from semiconductor M&A.