by Michael Hill

Point-of-sale (POS) vendors have built up an appetite for restaurant technology as the number of tech acquisitions they’ve made in that vertical has jumped since the start of the year. The uptick in these segment-specific deals arises from the food and hospitality industry’s penchant for embracing digital commerce innovation combined with weak overall demand for POS systems and software.

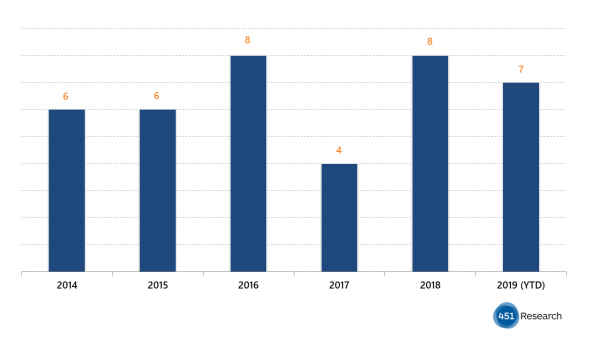

According to 451 Research‘s M&A KnowledgeBase, POS companies have inked seven restaurant tech purchases since the start of the year, almost as many as the eight they printed in 2018. Many of the acquisitions so far have been done to consolidate in the restaurant sector, while others were made to extend the buyers’ POS software suites into adjacent categories.

For example, restaurant POS startup Toast, which has amassed nearly $250m in funding since 2016, recently reached for StratEx, a provider of automated HR management software to restaurants that covers onboarding, payroll, benefits administration, scheduling, attendance and applicant tracking. As we noted in earlier coverage of Toast, the past few years have shown the food service segment to be among the earliest to embrace digital commerce innovations.

Restaurants have more advanced POS needs than the average retail business, demanding capabilities such as table management and online ordering, in addition to payment processing and customer management. And restaurants often spend more on POS systems than any other tech purchase, so nesting multiple applications inside these mission-critical systems offers a path to market for other restaurant-focused software products. HR management software such as StratEx’s aligns with restaurant POS, as that system doubles as a punch clock at most restaurants.

Other recent transactions appear to follow a similar recipe: start with POS and mix in other back-office applications. Take Lavu’s pickup of accounts payable specialist Sourcery Technologies earlier this month. With that move, the buyer is aiming to upsell restaurants with POS software that unifies restaurant sales with vendor management.

Part of the motivation for the string of deals in this space could be the modest growth for the overall POS market, which our surveys show is expected to be relatively flat in the coming months. According to 451 Research’s most recent Voice of the Enterprise: Customer Experience & Commerce, Organizational Dynamics & Budgets survey, only 42% of respondents said they expect their organization to maintain or increase its budget for POS software in the next quarter, the lowest reading for any of the nine software categories covered in the survey.

Annual acquisitions of restaurant technology vendors by POS providers