Contact: Scott Denne

Banking on the growth of the hybrid storage market, hungry investors sent Nimble Storage’s shares surging almost 50% above its IPO price for a market cap of $2.3bn in its first day as a public company. It is currently valued at a whopping 21.7x trailing sales.

Hybrid storage arrays like those Nimble sells combine flash and hard-disk drives in the same device, giving customers a better ratio of price to performance than traditional disk storage. Today the market is dominated by incumbents that have simply replaced disk drives with flash drives, rather than creating a new file system from scratch to accommodate both types, as Nimble has done.

A look at data collected by TheInfoPro, a service of 451 Research, shows that Nimble and its market are poised for more growth. This year the number of storage administrators who said they would spend more money on hybrid storage systems than they did a year earlier increased 27% compared with 18% who said the same thing last year.

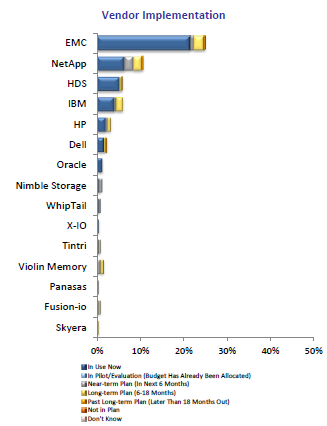

Our surveys also show Nimble accelerating within that market. While incumbents EMC and NetApp topped the list of vendors being implemented in the survey, Nimble was the highest ranked among the private, stand-alone companies. In 2012, it didn’t even get mentioned as a player in that category.

Continue reading “With a booming market ahead of it, Nimble’s IPO pops on day one”