by Scott Denne

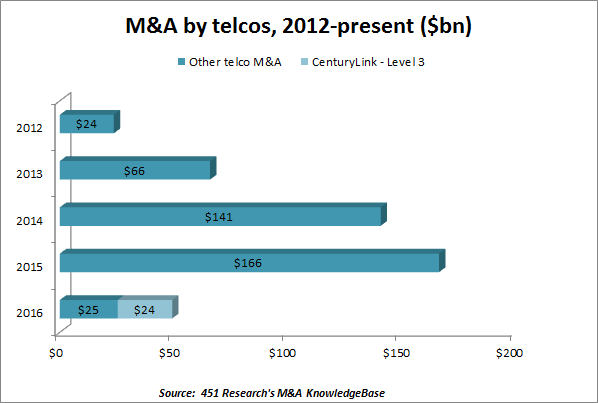

M&A activity among telcos is surging as phone, internet and wireless service providers increase both their buying and selling amid a general, though not complete, movement back toward their core markets after a streak of investments in ancillary tech sectors. Just this month alone, three carriers have unwound deals and scaled back their venture units. Still, acquisitions by carriers have hit their highest level since 2015.

According to 451 Research’s M&A KnowledgeBase, telcos have spent a collective $96bn on tech M&A this year, nearly four times the total spending among those acquirers in all of 2017. At the same time, publicly traded telcos have sold assets worth a combined $19.5bn, or twice the amount they sold in 2016 and 2017 combined.

Telstra is among the most recent sellers as it shed its $270m bet on Ooyala, a video streaming software vendor, in a sale to the company’s management. Alongside that transaction, it announced a restructuring of its venture arm, a move that reflects the recent decision by Rogers Communications to do the same. Telstra’s decision is part of a broader restructuring plan to cut costs and focus on customer service to return to growth (the Australia-based carrier’s topline declined 5% in each of the past two quarters).

Similarly, Sprint decided to divest its Pinsight Media unit in a sale to ad network InMobi. Like Telstra, Sprint is doubling down on telecom services – although in Sprint’s case, that’s taking the form of a $26.5bn sale to T-Mobile, a carrier that’s shown little appetite for moving beyond communications services. But that’s not to say that all carriers are sticking to the markets they know best.

Most notably, AT&T, following its massive $85bn pickup of Time Warner, has increased its acquisitions in digital media, ad-tech and even network security – its purchases of AppNexus and AlienVault account for more than half of the $3.6bn that telcos have spent this year on ancillary technologies. Given the recent failures of its competitors, not to mention the many abandoned forays into datacenters earlier in the decade, it’s tempting to take a dim view of bets in media and advertising.

Still, AT&T, as well as Comcast and Verizon – which made similar, earlier acquisitions in media and advertising – haven’t been the best stewards of their core businesses. There’s scant evidence to suggest that focusing strictly on their legacy business would be without its own risks. Multiple surveys by 451 Research’s VoCUL show consistently low levels of customer satisfaction among phone and TV service providers. For example, mobile services from Sprint and Verizon have trended down over the decade while AT&T has demonstrated little growth, with just 24% of customers saying they’re satisfied with the current service (only T-Mobile has posted long-term gains on that front).

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.

![Vonage_copy[1]](http://blogs.451research.com/techdeals/files/2016/05/Vonage_copy1.png)