by Michael Hill

Faster medical research, improved diagnosis and efficient patient monitoring were early and oft-touted examples of the changes that machine learning could bring. Despite that, there’s been little demand for acquisitions of machine learning vendors in the healthcare vertical. Or at least that was the case. This year, healthcare machine learning deals have suddenly accelerated as strategic buyers have begun seeking bolt-on acquisitions to keep up with customer demand.

According to 451 Research‘s M&A KnowledgeBase, nearly half of all machine learning purchases in the healthcare market have printed since the start of 2019. This year has seen 15 acquisitions of machine learning companies where the acquirer or target (often both) are selling into the healthcare vertical. Prior to this year, there hadn’t been more than six such deals in a single year.

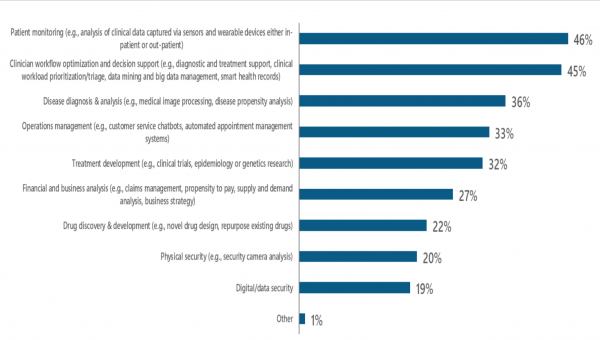

Healthcare machine learning transactions in 2019 have largely been characterized by a mix of veteran and first-time strategic buyers reaching for emerging tech targets to complement their existing offerings in line with their customers’ needs. For example, Royal Philips added Medumo’s machine learning patient monitoring software to its healthcare IT suite as a survey by 451 Research’s Voice of the Enterprise finds that ‘patient monitoring’ ranked at the top of multiple healthcare applications of machine learning, with 46% of healthcare respondents citing it as a use case for machine learning.

Nearly one of three survey respondents cited ‘clinical trials’ as an application of machine learning, which aligns with the rationales behind five of this year’s deals. And while the applications of machine learning in healthcare are coalescing, adoption remains nascent. Fewer than one of five healthcare providers claims to be using machine learning today.