by Scott Denne

Shopify has printed its first major acquisition, spending $450m in cash and stock for 6 River Systems. While the e-commerce technology vendor has inked a handful of tuck-ins, it hadn’t yet bought anything close to this size. In doing so, it joins a streak of new names to deliver significant VC exits this year. Although sales of startups are likely to fall below last year’s record haul, the emergence of new buyers has helped push exits for 2019 above a typical year.

According to 451 Research‘s M&A KnowledgeBase, 60% of venture-backed companies, including 6 River, that sold for $250m or more this year were bought by firms that had never paid that much for a startup. Some of this year’s buyers, including Shopify, Etsy and Uber, are youngish, growing businesses and former tech startups themselves Others are companies from more traditional industries that are new to acquiring tech providers, such as H&R Block with its reach for Wave Financial or McDonald’s, which bought Dynamic Yield in March.

Several others that have printed $250m-plus deals for venture-funded vendors this year only inked their first such purchase in 2018, including Blackstone Group, Palo Alto Networks and Splunk. The latter company printed its first $1bn-plus acquisition just last month, when it scooped up venture-funded SignalFx. Meanwhile, Palo Alto Networks has paid more than $1bn across four startup acquisitions in 2019.

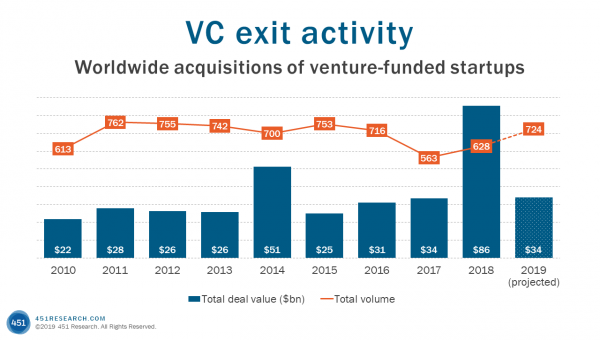

In 2018, new buyers accounted for just 40% of $250m-plus startup transactions. Still, there were far more $250m-plus VC exits last year – 63 compared with 24 so far in 2019. Although the number of significant exits and the total deal value of VC exits are down from last year, that’s hardly an alarming sign for the venture community. In 2018, venture-backed companies brought in a post-dot-com record $86bn via tech M&A. This year, they’re on track to bring in $34bn, higher than all but two years in the current decade (not to mention it’s coming alongside a booming IPO market), and the $9.5bn coming from new acquirers has played an outsized role in venture liquidity this year.

Figure 1