by Scott Denne

Last year marked a banner year for machine learning M&A. Purchases of vendors building products around that emerging technology, as well as firms whose offerings enable others to build machine learning products, soared in 2019. Yet the change was more than quantitative. As that new technology pervades older industries, it’s bringing in new acquirers and the rationale behind many machine learning deals has evolved.

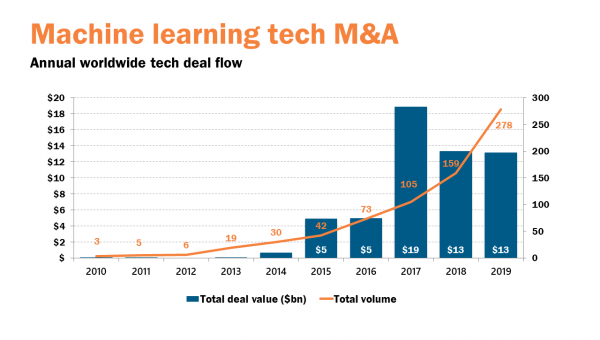

According to 451 Research‘s M&A KnowledgeBase, acquisitions of machine learning providers rose 75% to 278 in 2019. In other words, machine learning accounted for one of every 13 tech transactions last year. Within that number, purchases of companies selling into a specific vertical produced the most prominent rise as buyers nabbed 112 vendors building machine learning offerings that address problems within a particular industry, more than double the 53 they bought earlier.

In previous years, many acquirers were content to pick up general-purpose tech and expertise to bolster their machine learning portfolios. Serial shoppers Microsoft, Google, Salesforce and Apple, for instance, each picked up more than 10 businesses in recent years to expand their products’ machine learning functionality. As we previously noted, buyers have already become more discriminating, and more likely to seek tech that fills specific gaps in the product portfolio.

But the application of machine learning to certain markets has not only kept acquirer interest in the burgeoning technology high, it has also brought new buyers into the tech M&A market as staid industries see opportunities and risks that come with the emergence of machine learning. For example, in one of the largest machine learning deals last year, Prudential Financial printed its first tech acquisition with the $2.4bn pickup of Assurance IQ to expand its online sales via software that customizes insurance products around data signals.

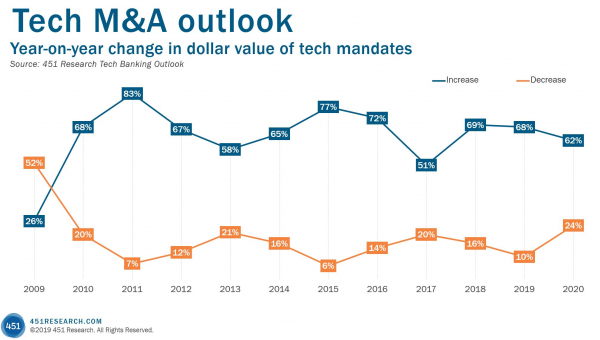

As the universe of buyers and the range of rationales for machine learning transactions continues to expand, this technology will likely continue to have an outsize impact on the tech M&A market. At least that’s the take from the 451 Research Tech Banking Outlook, where 91% of bankers surveyed anticipate that machine learning purchases will accelerate in 2020.

Figure 1: