by Scott Denne

Bill.com is looking to break a two-month dry spell of business technology IPOs as the SMB-focused payments software vendor unveils its prospectus. The offering comes as many other new listings have struggled to retain their momentum following frothy debuts, darkening the outlook for companies like Bill.com seeking to retain their unicorn status beyond their public offering.

With $121m in trailing revenue, Bill.com could come to market with a similar topline as PagerDuty, the IT management software firm that teed off this year’s round of enterprise IPOs back in April when the market valued it at 23x. Since then, its valuation has sunk to 10x, the multiple that Bill.com will need to fetch to retain the valuation from its last venture round. Landing a few turns higher seems doable, given that Bill.com’s sales grew 63% from a year earlier, compared with PagerDuty’s 47% (at the time of its IPO), and that the latter’s losses were more than three times larger than the $12m trailing net loss Bill.com posted.

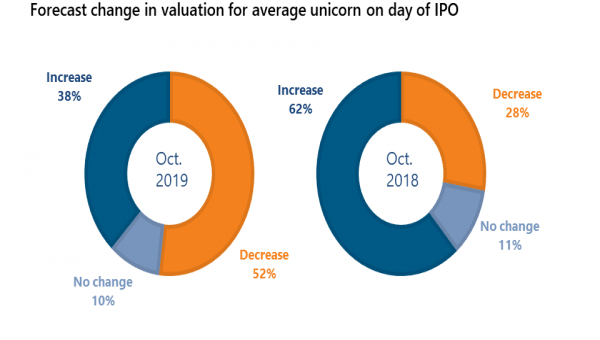

Still, the company will be running up against the expanding opinion that many privately held unicorns are overvalued. In the most recent M&A Leaders‘ Survey from 451 Research and Morrison & Foerster, 62% of respondents said they expect the average unicorn startup to carry a valuation on its first day of trading that’s flat or down from its last venture round. In the same survey a year earlier, only 39% predicted such an unwelcoming environment.

Figure 1: Expectations for unicorn debuts