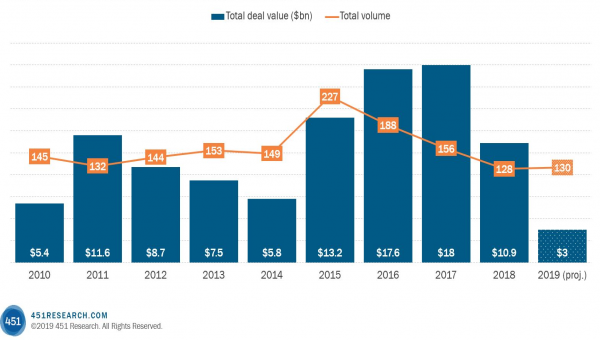

After bulking up in recent years in part to fend off the ever-expanding influence of the cloud suppliers, web hosting and managed service providers are now going it alone. For the most part, they’ve closed the M&A playbook, or at the very least, dramatically scaled back their acquisition ambitions. Deal spending this year is likely to slump to its lowest annual level since the recession a decade ago.

Based on the M&A pace through the first seven months of 2019, full-year spending on acquisitions in the hosting/managed services market is tracking to about $3bn, according to 451 Research’s M&A KnowledgeBase. Assuming the back half of 2019 plays out the way the year has gone so far, the value of announced transactions in the sector would be less than one-third the annual spending in any of the previous four years.

There are several reasons for the decline, including a few drivers that may be gone and not coming back. For starters, some of the biggest deals done by hosting and managed service providers in recent years were straightforward consolidations. Hosting companies were looking at their peers as a way to grab as much infrastructure (and as many customers) as possible and then wring out operational efficiencies.

However, with the rise of the cloud hyperscalers – providers that, collectively, spend billions of dollars a year on building and maintaining their clouds, and still have tens of billions of dollars in their treasuries – infrastructure became something of a commodity. For hosting firms, that has meant it’s no longer economical to acquire rivals to pile up infrastructure. Instead of buying, they are renting. Virtually all managed hosting vendors offer front-end management of cloud infrastructure from hyperscalers.

This shift in strategy isn’t only being driven from the supply side, however. A recent 451 Research survey of more than 700 IT buyers and users found that pricing was the key determinant of whether organizations used managed services. Slightly more than six out of 10 respondents (62%) told our Voiceof the Enterprise: Cloud, Hosting and Managed Services survey that lower costs were the main business case for managed services. That handily topped the half-dozen or so other benefits, which were all in the 40% range and below.

Figure 1: Hosted/managed services acquisition activity