by Brenon Daly

It’s never easy to make sense of Washington DC. And yet, the decisions made in the nation’s capital can dramatically shape the flow of business, often determining what can get bought and sold, along with who can do the buying and selling. That’s true for both products as well as the companies behind the products.

Consider the recent decision by the Federal Trade Commission (FTC) to block Edgewell’s proposed $1.3bn cash-and-stock purchase of online razor vendor Harry’s. The pairing of the old-line shaving giant, which sells its Schick and Edge offerings through traditional retail outlets, and Harry’s direct-to-consumer (D2C) product didn’t appear problematic when it was announced last May. After all, rival consumer package goods titan Unilever had closed a similar acquisition of Dollar Shave Club in mid-2016 in short order and without any hoopla.

The FTC’s move has huge implications for both this particular transaction and far beyond it. For Edgewell, the company has said it now expects to face litigation by Harry’s due to the broken deal, likely further increasing the cost of the once-planned, now-punted expansion. Further, as noted in S&P’s Capital IQ transcript of Edgewell’s most recent quarterly earnings report, the company is licking its wounds from the FTC decision, adding that it was ‘out of the market for big, transformational (acquisitions).’

The unanimous FTC decision surprised most M&A market observers. Buying a D2C startup as a way to expand a company’s distribution routes or decrease reliance on troubled traditional retail outlets has been a time-tested acquisition strategy. 451 Research‘s M&A KnowledgeBase lists more than 300 transactions that feature the term ‘direct to consumer,’ including deals by such household names as luggage maker Samsonite, cosmetic supplier Cody’s, mattress maker Serta and retailing titan Walmart, among others.

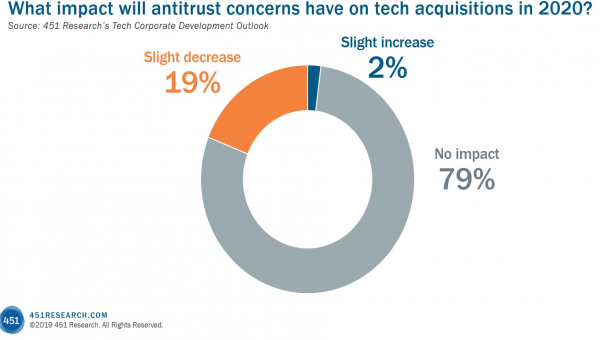

Further, most dealmakers told us they didn’t expect Washington DC to have much of an impact on their work in 2020. In the 451 Research Corporate Development Outlook last December, just one in five survey respondents indicated that they thought ‘antitrust concerns’ or broader regulatory review would lower the number of tech deals in the coming year. The overwhelming majority (79%) thought transactions such as Edgewell-Harry’s would move along as they pretty much always had.