by Brenon Daly

In addition to wrapping up a decade, 2019 also marked the end of an era in tech M&A. The industry’s longtime buyers are no longer buying like they did when they were in their prime. It was as if the old guard, having shaped and driven tech M&A for years, stepped aside as the curtain came down on the decade. Their departure has left a billion-dollar-sized hole in the market.

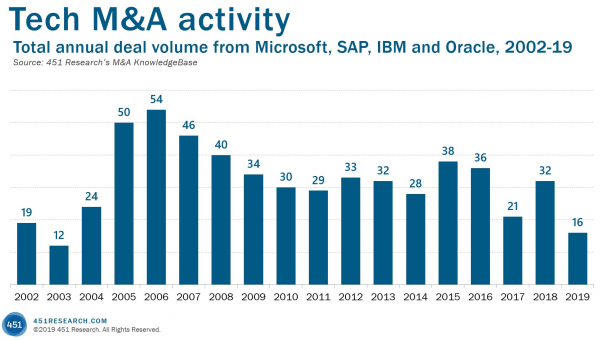

We noted this transition and its implications as a key market trend in our recently published M&A Outlook: Introduction. In the report, we highlight the fact that the 451 Research‘s M&A KnowledgeBase does not have a single transaction valued at more than $1bn for stalwart acquirers Microsoft, IBM, Oracle and SAP – the first time the group hasn’t had a single member in the ‘three-coma club’ since 2003. Our data indicates that the quartet, collectively, had been averaging almost four $1bn+ deals each year for the past decade and a half. (See our full report.)

The impact of the missing mainstays goes far beyond just the rarified top end of the M&A market. Not only are Microsoft, SAP, Oracle and IBM not putting up big prints, they are barely putting up any prints at all. According to the M&A KnowledgeBase, the quartet acquired a total of only 16 companies among them in 2019. That’s just half the number of purchases the four companies have averaged annually over the previous 15 years, and less than one-third the number they did in peak years.

Further, all four buyers have substantially more cash on hand and substantially higher stock prices right now than when they had their M&A machines revving. And yet, despite the unprecedented resources to do deals, their pace plummeted last year to each company averaging a transaction every quarter, down from an average of a purchase every month in the mid-2000s.

That slowdown has literally taken billions of dollars out of the broader tech M&A market. Our numbers show a staggering $262bn in total acquisition spending for Microsoft, IBM, Oracle and SAP since 2002. (The aggregate amount – again, more than a quarter-trillion dollars – captures only announced deal values and our proprietary estimates on prices, so undoubtedly undercounts the actual outlays from the four buyers.)

Even just based on the disclosed and estimated prices, the M&A KnowledgeBase shows the median deal value, collectively, for the quartet is $200m. Using the admittedly roughly measured representative price of $200m per transaction, we can put a price on their slowdown in dealmaking. If the quartet had merely announced the number of acquisitions in 2019 that they had averaged over the previous 15 years, another $3bn would have flowed into the tech M&A market last year.