Following two years of outsized spending, hosted services providers took a breather in 2018. M&A activity in the sector decreased across the board, as deal volume, aggregate spending and valuations all dropped, driven by a pullback among the largest hosting and multi-tenant datacenter (MTDC) providers. We expect the biggest buyers to return to heavier spending in 2019, fueled by the increasing need for infrastructure to support workloads in the cloud.

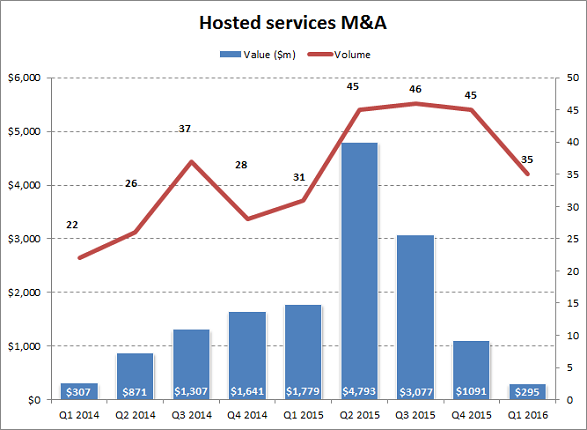

Despite a 23% drop in volume and 40% reduction in spending, hosted services M&A clocked its fourth consecutive year of more than $10bn in total value with $10.7bn. In the decade leading up to 2015, expenditures surpassed that benchmark just twice. And yet, the steep drop last year was jarring. According to 451 Research’s M&A KnowledgeBase, valuations also dropped – the median multiple on enterprise value to trailing revenue fell last year to 2.7x from 3.6x in 2017.

While overall tech M&A saw larger enterprises buying again, hosted services witnessed the opposite, with Digital Realty Trust and Equinix stepping back. From 2015 to 2017, those two buyers combined for about five acquisitions and $6bn in spending each year. In 2018, they inked two deals among them for less than half that typical amount. Digital Realty cited its muted share price as a reason for stepping back – both it and Equinix started 2018 with a dip, followed by a summer recovery and then ending the year down alongside the general markets.

Still, even with the decreased spending, Digital Realty Trust and Equinix inked two of the year’s most notable hosting deals. Digital’s $1.8bn purchase of Ascenty gives it a strong foothold in Latin America, while Equinix’s $800m pickup of Infomart Dallas highlights the company’s continued efforts to extend its interconnection reach. Setting aside those two buyers, both financial and strategic acquirers each reduced spending more than 20%.

Exacerbating the decline, hosted services companies are less likely to buy their peers, and have increasingly looked to other markets for growth, particularly managed services, while they aim to move up the stack as their customers increasingly opt for cloud over datacenter deployments. In 2018, hosted services companies purchased 19 IT services and outsourcing business, compared to 13 in 2017. In that vein, we saw deals such as Rackspace buying Salesforce cloud integrator RelationEdge, and eHosting acquiring Microsoft cloud MSP LiveRoute.