by Brenon Daly

In sports, the old joke goes that to be successful, athletes need to pick their parents wisely. In much the same way, to be successful, tech startups not only need to pick their parents wisely, but also their birthdate. Demographics are destiny, at least when it comes to exits.

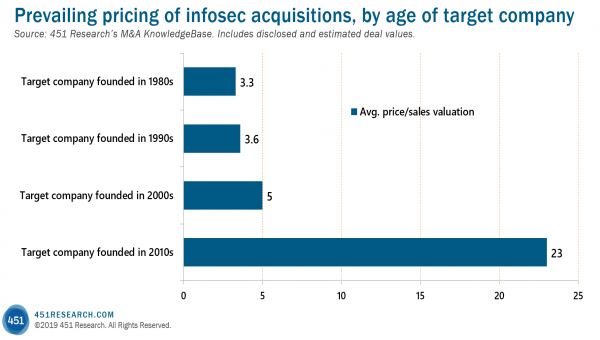

Consider the prevailing acquisition valuations for different age groups of information security (infosec) vendors in 451 Research‘s M&A KnowledgeBase. (To be clear, the deals are sorted by the founding date of the target, regardless of when the transaction was announced. Our data covers all infosec sectors going back to 2002.) The conclusion: When a company comes to market goes a long way toward determining what it’ll be worth when it leaves the market.

Infosec providers born in the 1980s, on average, garnered 3.3x trailing revenue when they sold. Representative transactions of that vintage include big platform deals such as Symantec’s blockbuster sale of its enterprise security unit to Broadcom (4.5x) and the just-printed carve-out of RSA Security from Dell. (M&A KnowledgeBase subscribers can see our estimated terms for the most recent RSA transaction.)

Similarly, infosec vendors dating back to the 1990s were valued at an average 3.6x trailing revenue in their sales. For these ‘tweener’ companies – not quite massive platforms, not quite sprightly startups – we would point to the Avast Software-AVG Technologies consolidation (3.2x) and Webroot’s sale to Carbonite (2.9x) a year ago.

Valuations ticked higher for companies founded in the first decade of the current millennium. Our data shows this ‘teenage’ cohort got valued at 5x trailing sales. Deals include the recent take-private of ForeScout Technologies (5.5x) and our estimate of terms on AlienVault‘s sale to AT&T in mid-2018.

By far, however, the youngest vendors fetched the richest pricing. Companies born in just the past decade pocketed, on average, a stunning 23x sales when they exited. Boosting this valuation are the half-dozen startups acquired recently by Palo Alto Networks as well as Phantom‘s high-priced sale to Splunk, according to our understanding.

Of course, we would intuitively expect younger, less-developed companies to enjoy higher relative valuations, if just because of basic math. (In price/sales multiples, small denominators yield larger end results.) But that doesn’t fully account for the tremendous M&A premium lavished on the youngest startups. There’s also the allure of youth, which changes the calculation as well.

With their limited history, startups focus on the future. Extrapolating from early successes, these up-and-to-the-right startups are convinced that their businesses will only know success, that they will always have a triple-digit growth rate. Naturally, when it comes time to sell, fast-growing startups expect to be rewarded. That’s true even – or, especially – if their financials are more aspirational than actual.