by Brenon Daly

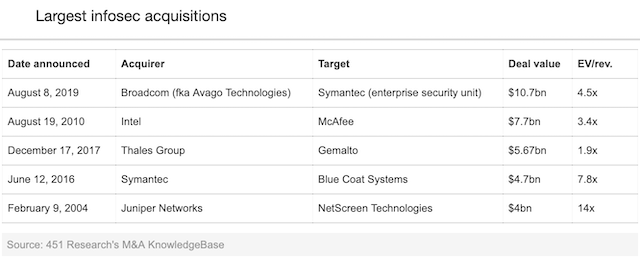

What began last summer as a head-scratching novelty has now become a consistent strategy at chipmaker-turned-software vendor Broadcom. A year after the semiconductor giant inked the second-largest software acquisition in history, Broadcom has made a big splash in information security (infosec), paying $10.7bn for Symantec’s enterprise security business.

Although the transaction is ‘just’ an asset purchase, it nonetheless stands as the largest infosec acquisition in history, according to 451 Research’s M&A KnowledgeBase. Another way to look at it: Broadcom’s massive bet on Symantec basically equals a full year’s worth of M&A spending for the entire infosec market. (The M&A KnowledgeBase shows annual spending across the infosec sector over the past two decades has ranged widely from $2bn to $28bn, depending on blockbuster deals.)

By virtually any measure, Broadcom is paying up for Symantec’s castoff business. Divestitures, particularly those involving low- or no-growth businesses, invariably garner a discount to broad-market M&A multiples. Depending on the segment and the assets, divestitures can get done at 1-2x sales, or half the prevailing prices in outright acquisitions.

At a purchase price of more than $10bn, Broadcom is valuing the enterprise security division at 4.5x sales. (In the most-recent fiscal year, Symantec’s enterprise group posted sales of $2.4bn, a level that hasn’t really changed in three years.) That’s even slightly richer than the 4.3x that Broadcom paid in its landmark acquisition last summer of CA Technologies.

The most-significant portion of Symantec falling into the portfolio of a financially minded consolidator comes after a prolonged slump at Big Yellow, which has served – not entirely fairly – as a company caught on the wrong side of disruption. As one indicator, consider that its stock price has basically been stuck in place for the past half-decade. During that same period, other business-focused security vendors have emerged and created somewhere in the neighborhood of $100bn – or 10x the terminal value of Symantec’s enterprise business – in both the public and private markets. We’ll have a full report on this transaction for subscribers to 451 Research’s Market Insight service later today.