Contact: Brenon Daly

With sharp elbows and deep pockets, private equity (PE) shops have announced more deals so far this year than the opening quarter to any year since the end of the recent recession. Already in 2017, 451 Research’s M&A KnowledgeBase has tallied 165 transactions by PE firms and their portfolio companies, a 15% jump from the previous record in Q1 2016. More broadly, buyout shops are currently about twice as busy as they were just a half-decade ago. Cash-rich financial acquirers represent the only significant group that’s accelerating activity in an otherwise slowing tech M&A market.

The dramatic surge in PE activity is primarily due to the ever-deepening pool of financial buyers. In the history of the industry, there have never been more tech-focused buyout shops that have had access to more capital, collectively, than right now. New firms have popped up while existing shops have put even more money to work in the tech industry, which is becoming even more ‘target rich’ as it ages. For instance, both Clearlake Capital Group and TA Associates have already announced as many deals in 2017 as each of the firms would typically print in an entire year.

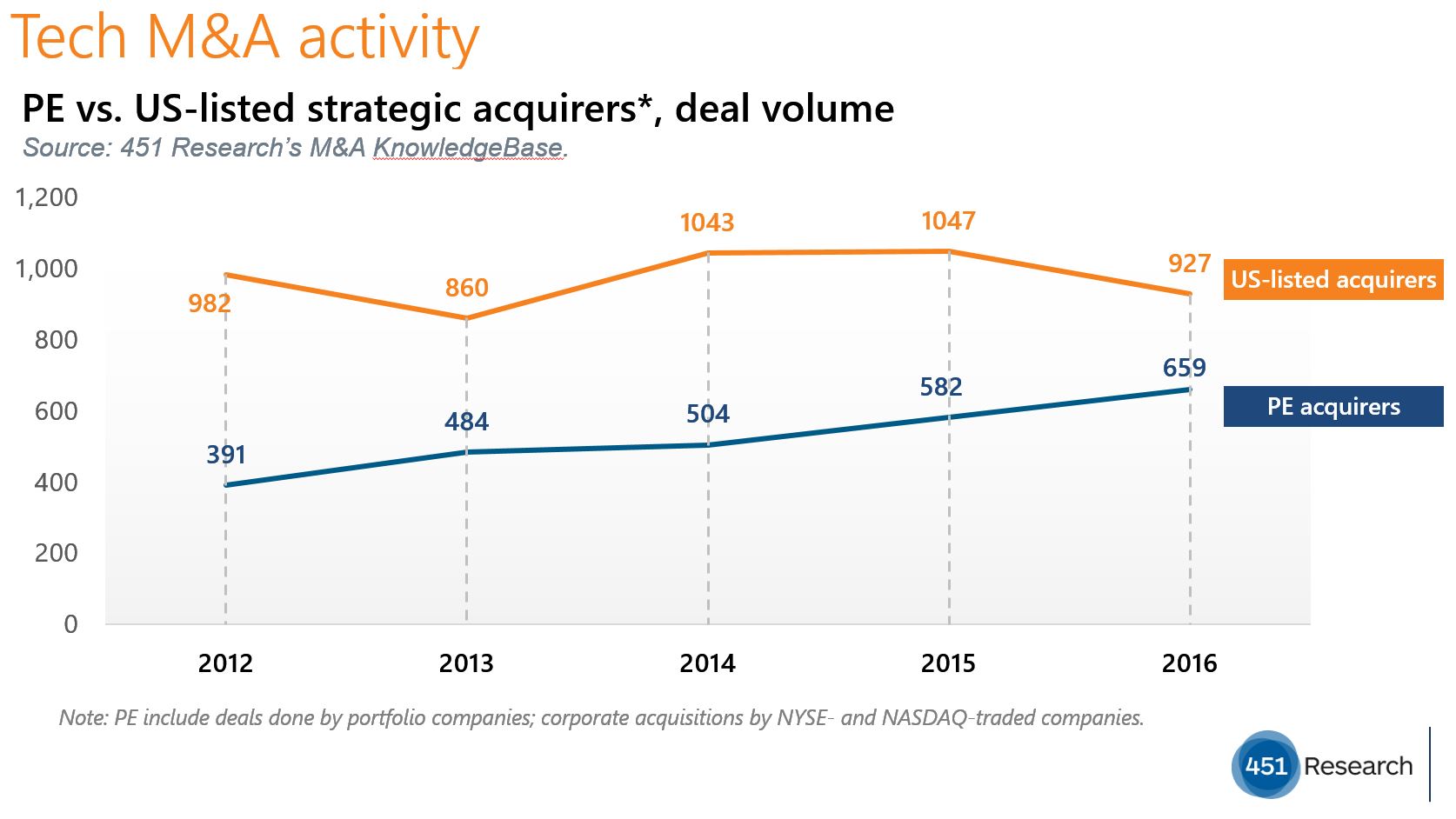

Of course, merely having record amounts of money doesn’t necessarily mean that firms will do more shopping. After all, that hasn’t been seen among corporate acquirers, which stand as the main rivals to PE shops. Tech companies that trade on the NYSE and Nasdaq have never had fatter treasuries than they do now, but the number of acquisitions they announced in 2016 dropped 11% compared with 2015, according to the M&A KnowledgeBase. In contrast, PE firms registered almost exactly the inverse, with the number of transactions increasing 13% in 2016 from 2015.

As financial acquirers step up their activity and strategic buyers step back, the once-yawning gap between the rival buying groups is narrowing. In the years immediately after the recent recession, tech companies listed on US exchanges regularly put up twice as many prints as PE firms. However, for full-year 2016 and so far in 2017, M&A volume for corporate acquirers is only about 30% higher than their financial rivals, according to the M&A KnowledgeBase.