Contact: Brenon Daly

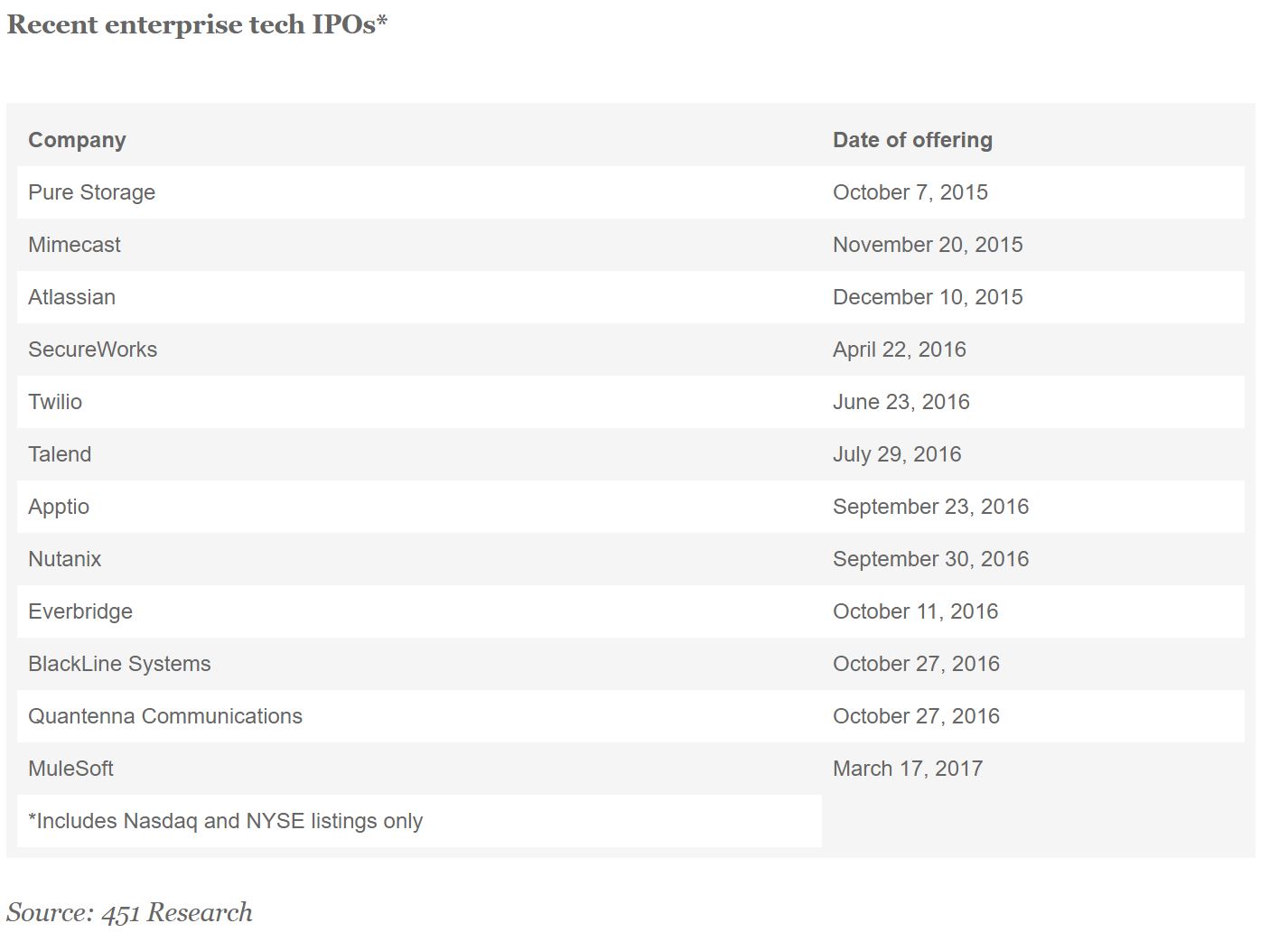

Data analytics vendor Alteryx has made its way to Wall Street, the second enterprise software provider to go public in as many weeks. The IPO, which raised $126m for the company, comes on the heels of a more-ebullient offering from MuleSoft. Together, the two oversubscribed IPOs indicate that the market for new offerings has rebounded from this time last year, when not a single a tech company made it public until late April.

Alteryx priced its shares at $14 each, and then edged higher to $15.50 on the NYSE during afternoon trading. With roughly 58 million (non-diluted) shares outstanding, the company is valued at about $900m. While MuleSoft more than doubled its private market valuation when it hit Wall Street, Alteryx’s IPO pricing is only slightly above the level it last sold shares to private investors in September 2015.

Although Alteryx debuted at a more modest valuation compared with MuleSoft, it did secure a double-digit multiple, albeit barely. Wall Street is valuing Alteryx, which recorded $86m in revenue last year, at 10 times trailing sales. That compares with about 16x for MuleSoft in its debut. The reason for the discrepancy? MuleSoft is more than twice as big and growing faster, increasing 2016 revenue by 71% compared with the 59% year-over-year growth for Alteryx. (Whether the comparison between the two vendors is fair or not, it is perhaps inevitable given the timing of their IPOs.)

In terms of future growth, Alteryx does face some challenges, as we have noted. Currently, the company focuses primarily on transforming and cleansing data and analyzing it using a combination of internally developed algorithms and functions based on the R open source computing statistical computing environment. Its own visualization and discovery capabilities are rather limited. Alteryx partners with Tableau, Qlik and Microsoft (Power BI) for this technology.

However, this partnership strategy could inhibit the company’s future expansion because visualization and data discovery are useful for attracting less-technical end users, which it will need to do to increase the number of users of its technology. Right now, Alteryx’s users are largely data analysts even though the company markets itself as a self-service data analytics vendor for technical and nontechnical end users.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.