Contact: Ben Kolada

There’s no denying that behavior in the equity markets is one of the main influencers on big-ticket M&A. Stock market stability provides a vote of confidence for corporate acquirers to pursue large, game-changing deals. Without stable markets, the valuation gap between buyers and sellers becomes too wide for potential sellers to accept. As a result, when the equity markets dip, so too does deal volume.

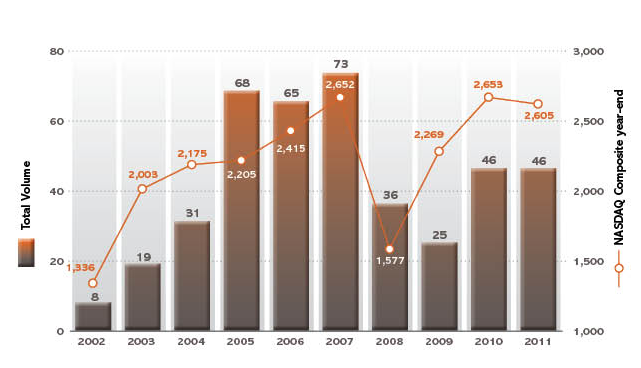

Nearly every drop in the tech-heavy Nasdaq Composite stock index coincided with a drop in both the volume and value of acquisitions of publicly traded technology companies. (Note: we’ve limited the scope of this research to the acquisition of Nasdaq- and NYSE-listed companies valued at more than $250m.) The number of acquisitions of large public companies tracks the stock market so closely that while the Nasdaq ended 2011 basically flat from the prior year, so too did the number of large tech transactions.

Public company acquisitions relative to Nasdaq activity

Source: The 451 M&A KnowledgeBase, 451 Research

By early 2012, the Nasdaq had effectively regained the level it held before the credit crisis. Despite this bull run, however, there’s very little certainty or stability in the equity markets. Although not a flawless metric, we can use predictions for the IPO market as a gauge of 2012 activity. A stable stock market is desired before a private company hits the public stage. According to our 2011 Tech Banking Outlook Survey, which forecasts activity for 2012, bankers expect the public markets to be stable enough to welcome 25 new technology firms this year – the same number predicted for 2011.

But the number of IPOs is only half of the equation, as subsequent stock performance shows longer-term confidence in the newly public companies’ businesses. In 2011, we saw a number of fairly successful tech IPOs, many of which came from the consumer technology sector, such as LinkedIn and Zynga. But some of these vendors’ initial good fortunes were short-lived. LinkedIn, for example, has lost one-quarter of its market value since the company debuted in May 2011, and Zynga is trading below its offer price.

Among the top issues affecting stock markets are progress toward resolving or containing the European debt crisis and an agreement by the US congress on a bipartisan plan that would reduce the federal deficit by at least $1.3 trillion over the next 10 years. A full 85% of tech bankers surveyed answered that progress on the European debt crisis would increase M&A activity, while 73% said the same about progress on reducing the federal deficit. However, neither of these issues seems likely to be resolved anytime soon. The European sovereign debt crisis appears particularly hairy, after credit rating agency Standard & Poor’s recently downgraded nine major European nations’ credit ratings. Meanwhile, presidential election season in the US is likely to cause most to focus on campaigning rather than the federal deficit. While many weigh their options in voting for the next US president, the stock market may lose its vote of confidence, and deal volume could decline as a result.