Contact: Brenon Daly

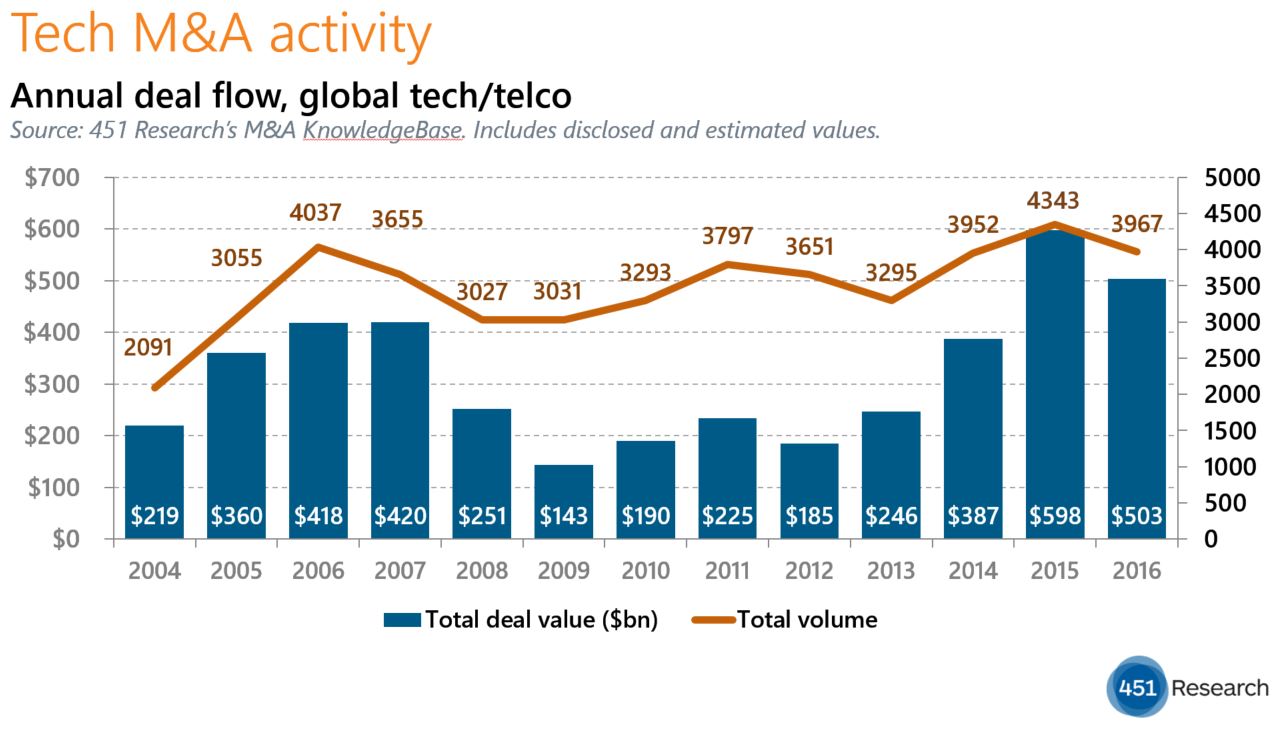

The tech M&A market is still struggling to get going in 2017. For the second straight month, spending on tech acquisitions around the globe totaled just half the average monthly level from last year. According to 451 Research’s M&A KnowledgeBase, tech acquirers announced just $19bn worth of transactions in the just-completed month of February, almost exactly matching the low spending level of January. Put together, the opening months of this year represent the weakest back-to-back monthly spending totals since 2013.

Similarly, the number of announced deals in February slumped to its lowest monthly level in more than three years. The 238 transactions tallied for February in the M&A KnowledgeBase represents a 30% slide from January deal volume and a 25% year-over-year decline from the average activity levels in February 2016 and February 2015.

The decline is due primarily to several of the well-known corporate acquirers either slowing their M&A machines or unplugging them altogether so far this year. For instance, neither SAP nor Intel have put up a 2017 print. Meanwhile, IBM has announced just one small transaction this year, down from a head-spinning pace of seven acquisitions in the first two months of 2016.

On the other hand, private equity (PE) firms have continued their record-setting pace. Buyout shops, which represent the sole ‘growth market’ in tech M&A right now, announced 23 deals in February – almost as many as they did in February 2015 and February 2016 combined. Three separate PE firms (Blackstone Group, H.I.G. Capital and The Riverside Company) announced at least two transactions last month.

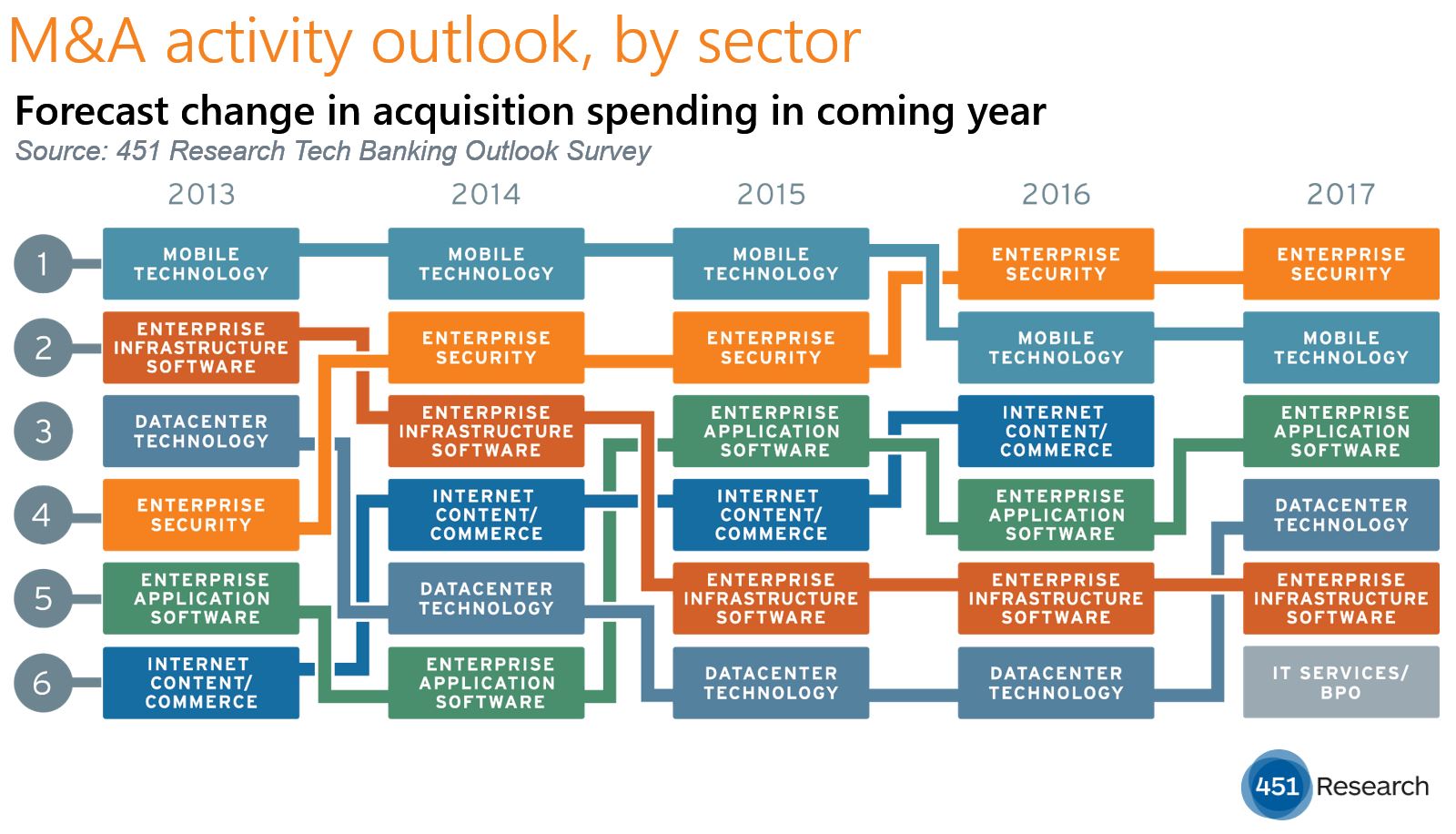

The lackluster start to 2017 comes after tech M&A hit its two strongest years of the past decade and a half. (Tech acquirers dropped more than $1.1 trillion on deals over the 2015-16 spree, according to the M&A KnowledgeBase.) That recent record activity appears to have siphoned off some of the acquisitions in 2017. Senior tech investment bankers surveyed by 451 Research last December gave their weakest forecast for M&A spending in 2017 for any year since the recent recession.