-by Brenon Daly, Christian Renaud

Announcing its largest-ever acquisition, private equity (PE) firm Thoma Bravo says it will pay $3.6bn for Riverbed. The take-private of the WAN optimization vendor comes after more than a year of pressure from activist hedge fund Elliott Management. Under terms, Thoma, which has a history of profitably acquiring infrastructure software providers, will hand over $21 for each of the roughly 170 million fully diluted Riverbed shares.

Thoma Bravo is valuing Riverbed at 3.4x the $1bn that the company has put up over the past year. (Sales growth has been underwhelming so far in 2014. Through the first three quarters of the year, Riverbed inched up its top line by 6% – just one-quarter the growth rate from full-year 2013.) The valuation is roughly in line with other recent significant take-privates such as Thoma’s leveraged buyout of Compuware and Vista Equity Partners’ LBO of TIBCO Software.

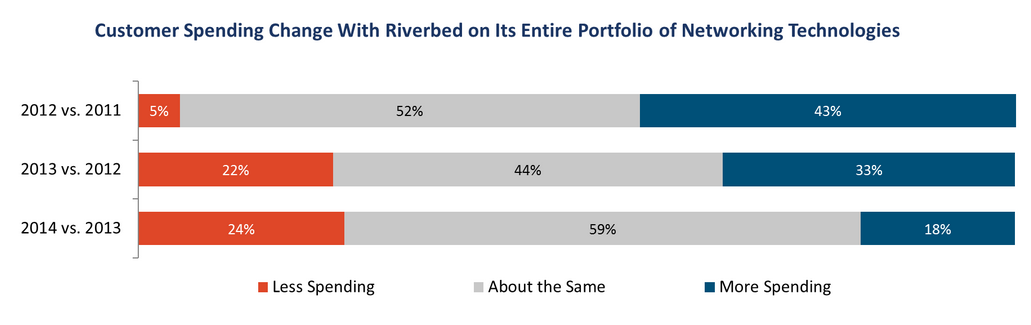

The primary reason why Riverbed’s growth has stalled – which precipitated the initial unsolicited approach from Elliott – is the considerable changes in market requirements (greater demand for traffic analysis and grooming) and enterprise networking (evolution to cloud-delivered services). A study by TheInfoPro, a service of 451 Research, earlier this year indicated that more customers were planning to cut their spending with Riverbed in 2014 than increase their spending with the vendor. We’ll have a full report on this transaction in tomorrow’s 451 Market Insight.