Contact: Brenon Daly

After a surprisingly strong year for tech M&A spending in 2016, it’s natural to look ahead to this year and wonder how – and where – dealmaking will play out. To get a sense of that, we asked the primary players in the market for their specific forecasts on acquisition activity, valuations and even IPOs. 451 Research subscribers can see the full report on our tenth-annual 451 Research Tech Corporate Development Outlook Survey, as well as our twelfth-annual 451 Research Tech Banking Outlook Survey.

In addition to both survey groups offering their broad forecasts for tech M&A, we also asked specific questions about topics that will undoubtedly shape the market in the coming year. A quick highlight from each of the surveys:

- A plurality of corporate acquirers are anticipating a ‘Trump rally’ in the tech M&A market in 2017. Half of the respondents (49%) expect the political and economic changes from the president-elect’s policies to ‘stimulate’ M&A activity – three times the percentage (16%) that said the policies will ‘inhibit’ dealmaking in the coming year.

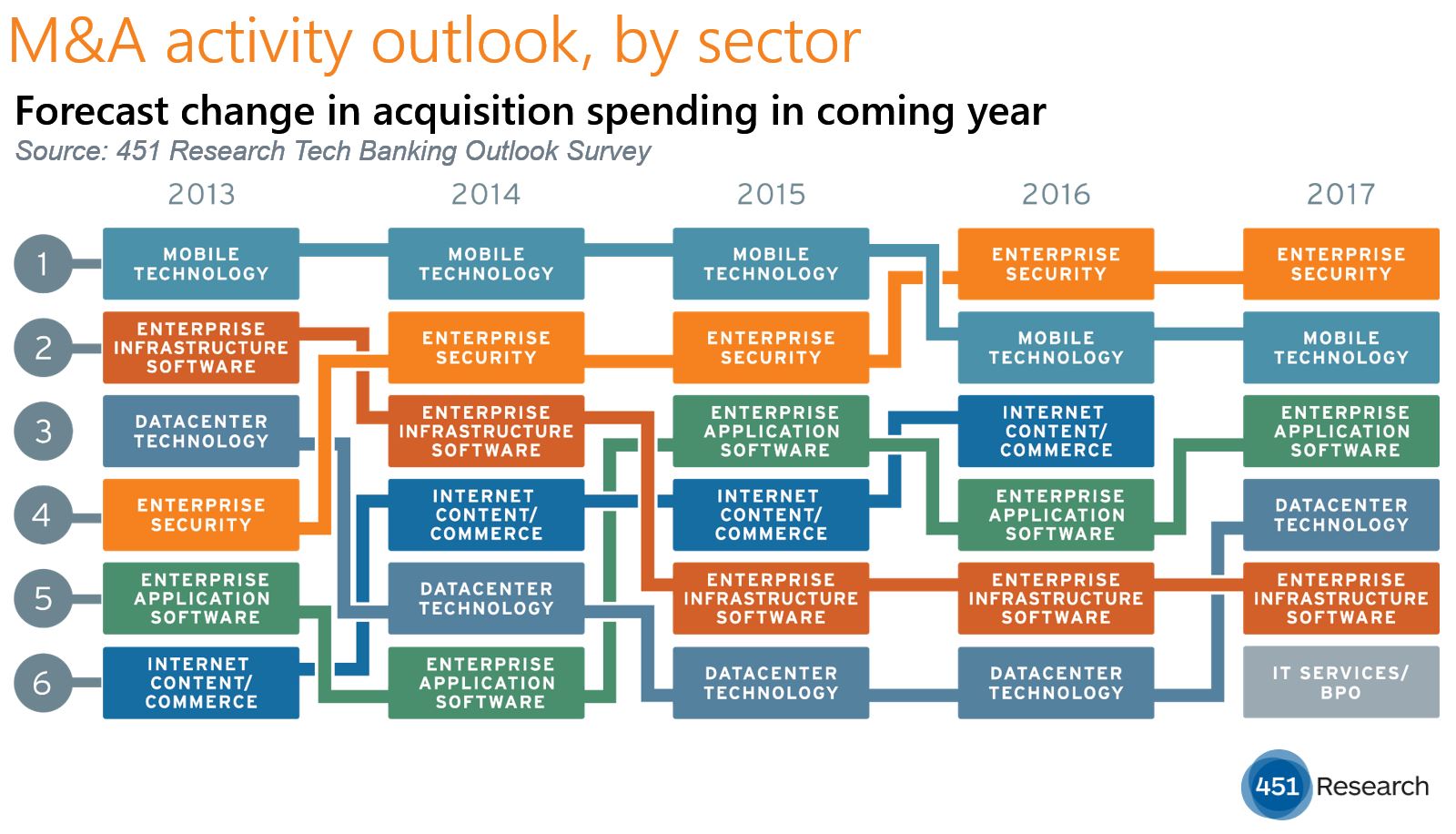

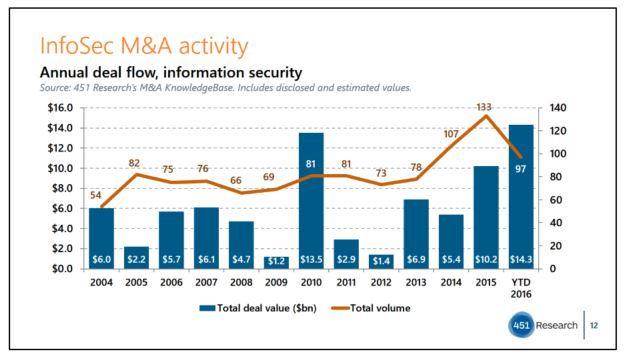

- Tech bankers expect even more M&A spending on enterprise security in the coming year. They also picked that as the top sector for 2016, and they were on to something: Spending on enterprise security soared to a record $16.7bn, more than the two previous years combined, according to 451 Research’s M&A KnowledgeBase.

Again, to see our full report on the M&A outlook from many of the most-active corporate acquirers, click here; and to see our full report on the views and predictions from senior tech investment bankers, click here.