Contact: Ben Kolada

Facebook’s stratospheric growth has had a profound impact on technology entrepreneurship and exits. In addition to creating some $60bn of market value in its own recent IPO, the company has spawned an ecosystem of vendors hoping to further monetize its one billion customers. A myriad of startups have popped up over the years to help advertisers, marketers and brands manage and deliver their message across Facebook’s platform, which some bulls on the company consider something like a new operating system.

Several of these startups are finally starting to show material sales. As a result, the market overall is being targeted by tech titans looking to become advertising and marketing vendors of choice for agencies and brands. That has led to a dramatic rise in the volume of acquisitions of tech firms serving this segment. Last year set the record in both the volume and value of acquisitions.

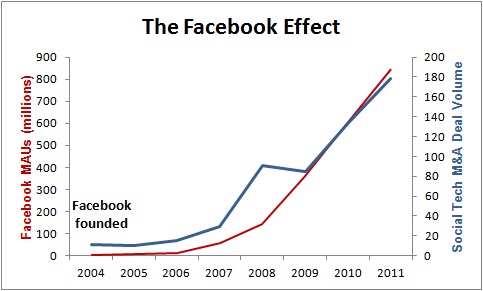

Dealmaking this year, however, has already shattered that total spending record: The $3.6bn spent so far this year on social-related companies is already twice the 2011 total. The M&A is being driven by phenomenal growth rates in the social media market. As a proxy for that, consider Facebook’s monthly active user (MAU) count, which has grown at a compound annual growth rate of 132% from its founding in 2004 to 2011.

The social media sector’s growth is leading to top-dollar prices for hot startups. Buddy Media, probably the largest social media marketing platform vendor, increased revenue 250% last year. On Monday, salesforce.com officially announced that it is paying $689m for Buddy Media. Meanwhile, Google and Meebo made their pairing official: Google is reportedly paying $100m for the social networking and user engagement vendor. Oracle just paid an estimated $325m for social marketing provider Vitrue to gain capabilities competitive to what Buddy Media offers. (And the enterprise software giant tucked in Collective Intellect for social media monitoring on Tuesday.) And finally, even old-line vendor IBM has inked a high-priced deal in the market, likely paying north of $200m for social sentiment provider Tealeaf Technology last month.