Contact: Scott Denne

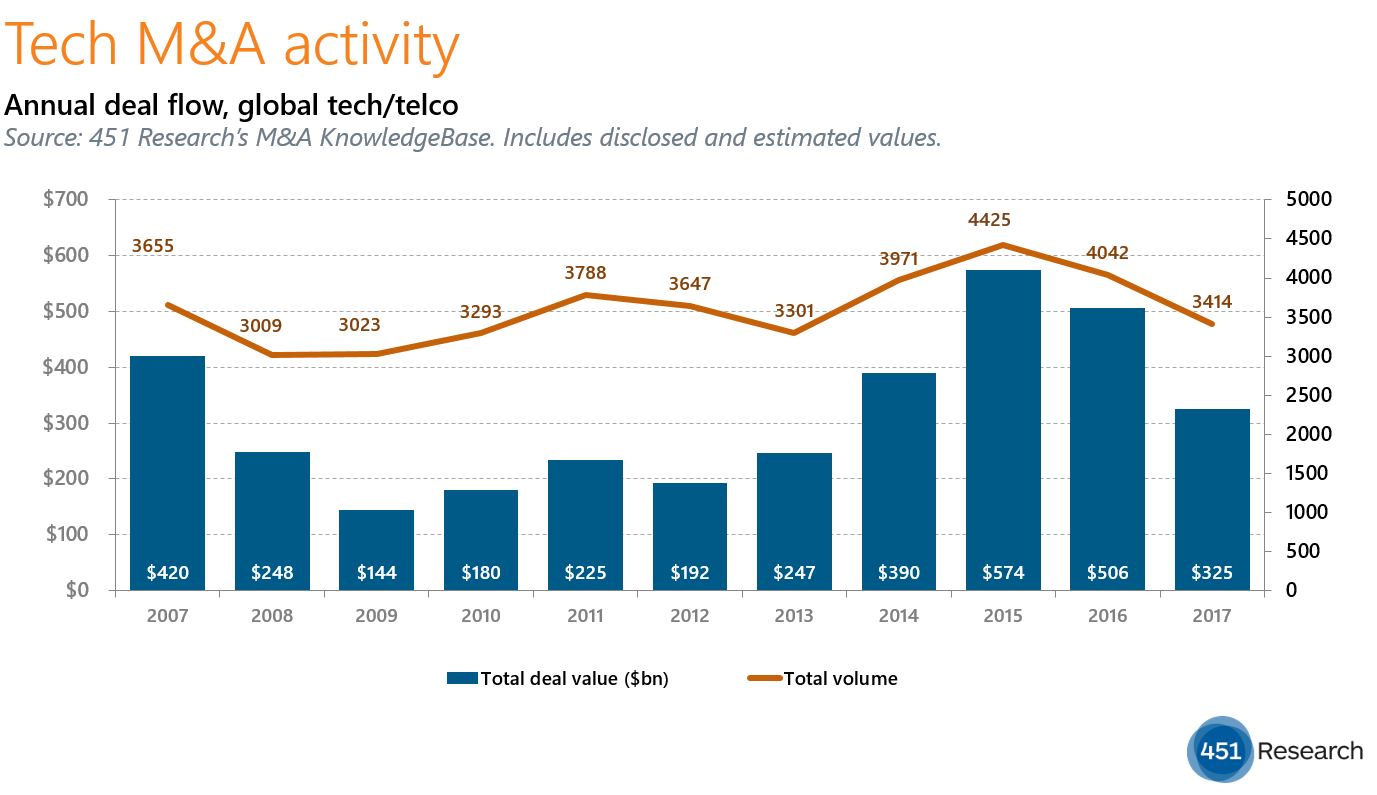

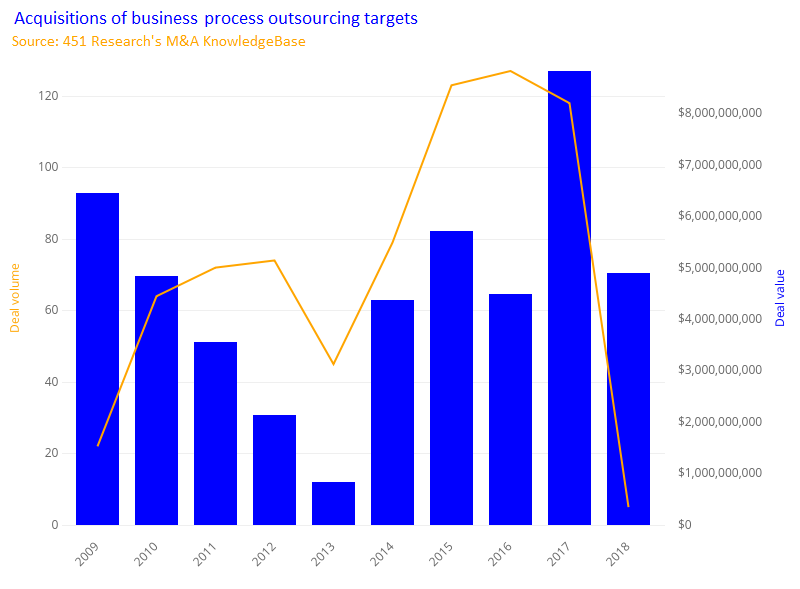

Business process outsourcing (BPO) deals jumped to a record total in 2017, despite an overall decline in tech M&A. Today’s announcement that SS&C Technologies will buy its competitor, DST Systems, for $4.9bn sets up the category for another big year.

According to 451 Research’s M&A KnowledgeBase, BPO targets fetched $8.8bn, double the previous year’s total, as the sector saw more big-ticket purchases. That trend continues with the sale of DST, a provider of software and services to investment and wealth management companies, which marks the largest BPO transaction since Xerox’s 2009 pickup of ACS for $6.4bn. With today’s acquisition, there have now been nine BPO deals valued above $1bn in the past decade. Five of them have come in the past 18 months.

SS&C’s purchase values DST at $5.4bn, or 2.7x trailing revenue, a multiple that’s lower than SS&C’s two previous largest acquisitions – Advent Software ($2.5bn) and GlobeOp ($895m). A heftier services offering and slimmer margins are likely to blame for the difference in multiple – SS&C had a 15% operating margin last quarter, compared with DST’s 10%.

Still, DST is commanding a premium that’s well above that of a typical BPO vendor, continuing a trend of rising valuations in the space. According to the M&A KnowledgeBase, the median multiple among BPO targets last year was 2.4x, a number that in itself was extraordinary seeing as the median multiple for such transactions rarely clocks in above 1x in any given year.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.