Contact: Brenon Daly

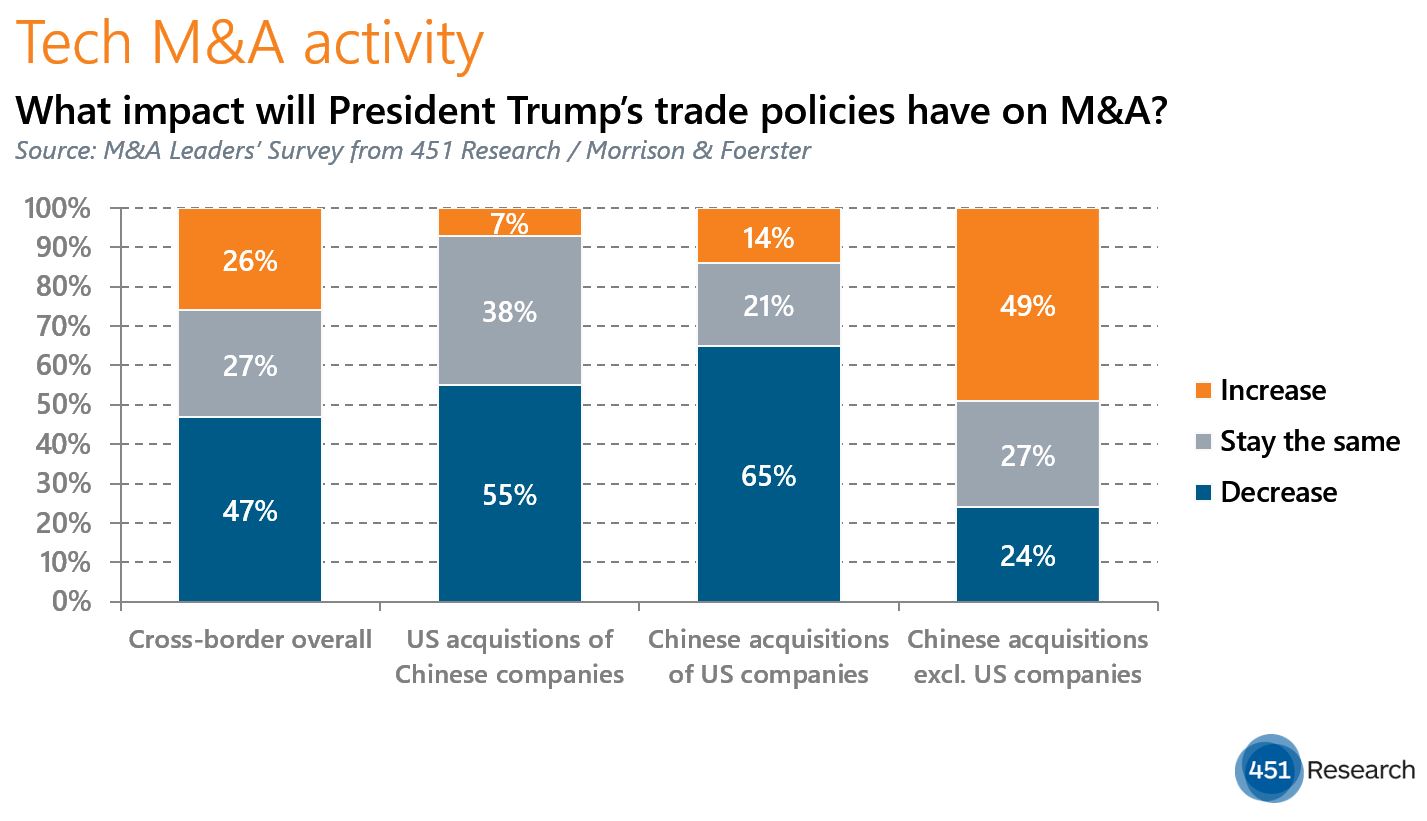

Respondents to the previous edition of the M&A Leaders’ Survey from 451 Research and Morrison & Foerster have once again delivered the wisdom of the crowds. When asked last spring about the outlook for US-China tech deal flow, respondents overwhelmingly predicted that President Trump’s policies would crimp M&A activity between the world’s two largest economies. Specifically, two-thirds (65%) of the 157 respondents from across the tech M&A landscape forecast a decline in purchases of US tech companies by Chinese buyers. That was more than four times the level (14%) that anticipated an increase.

In line with that April forecast, Trump has blocked the proposed $1.3bn acquisition of Lattice Semiconductor by a Beijing-based fund, citing national security concerns. Regulatory approval of the planned purchase by Canyon Bridge Capital Partners, which was announced last November, had been viewed as virtually impossible after The Committee on Foreign Investment in the US indicated that it would not sign off on the transaction. Trump delivered the death blow to the deal on Wednesday.

Trump’s move represents a rare bit of White House intercession in an acquisition. But it isn’t necessarily out of character for Trump, who has singled out China for some of his sharpest criticism as he has pursued a self-described ‘America First’ policy. Again, respondents to the M&A Leaders’ Survey last spring accurately predicted that Trump’s singularly unfriendly views toward China would disproportionately impact US-Sino deal flow. In the survey, fully one out of five respondents (20%) forecast that Chinese buyers of US tech companies, such as Lattice Semi, would ‘substantially’ cut their activity due to the Trump administration, compared with just 3% who said they expected overall cross-border M&A to drop off ‘substantially’ in the current regime.

451 Research and Morrison & Foerster are currently in market with the latest edition of the M&A Leaders’ Survey, and would appreciate your views on where the tech M&A market is and where it’s heading. In addition to broad market questions, we also revisit questions around Trump’s impact on cross-border M&A as well the specific outlook for China-based buyers. We would appreciate your time and thoughts. To participate, simply click here.