Contact: Brenon Daly

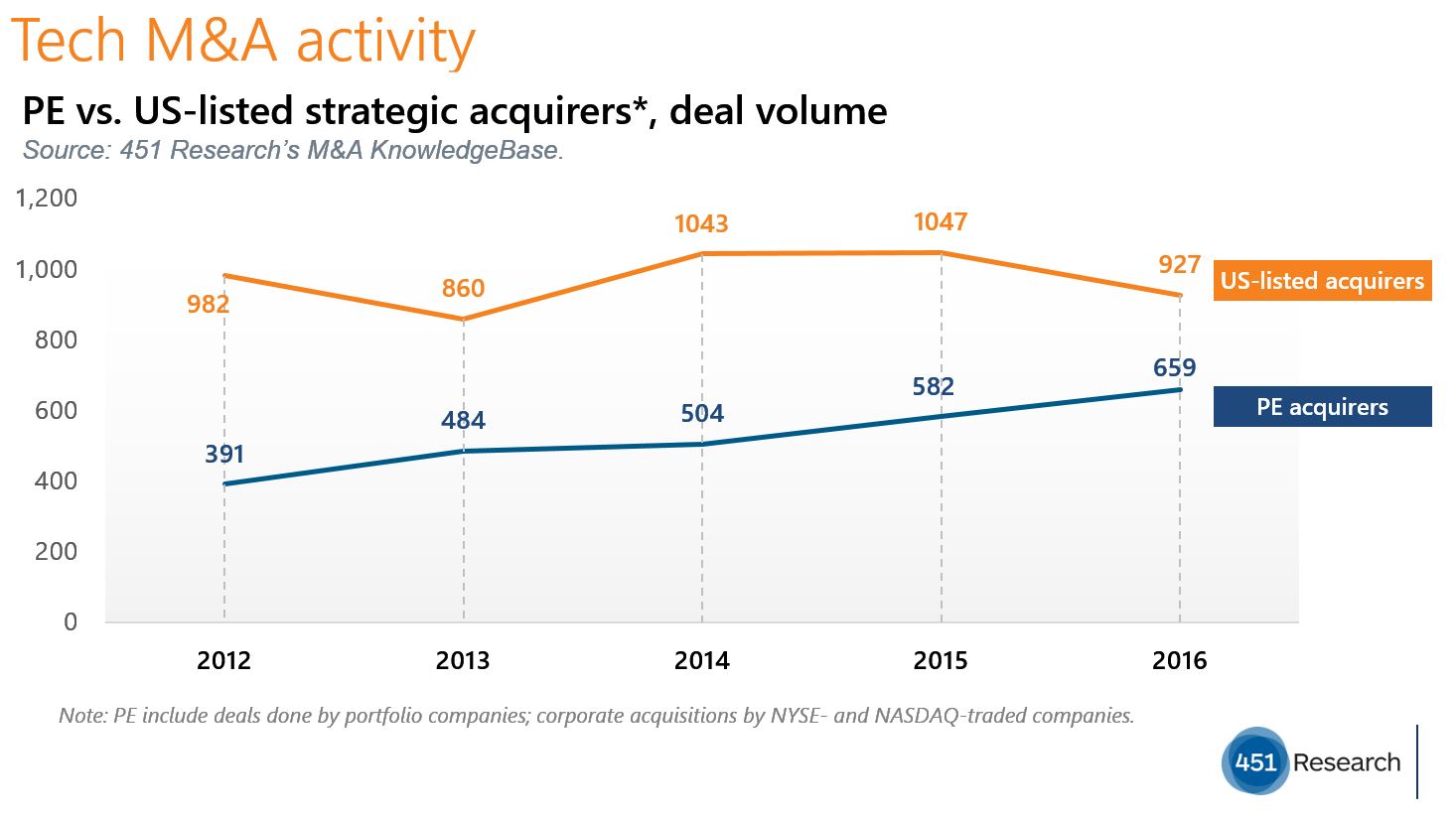

For the first time in tech M&A, financial acquirers are doing more deals than publicly traded strategic buyers. That’s a sharp reversal from years past, when private equity (PE) firms represented only bit players in the market, operating well outside the focus areas of US-listed acquirers. Even as recently as three years ago, US publicly traded companies were announcing more than twice as many transactions as PE shops.

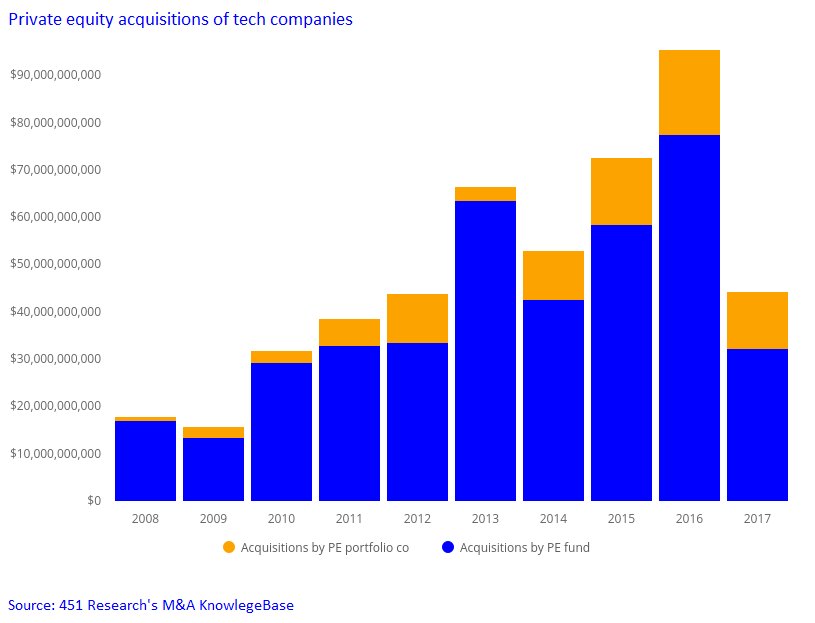

So far in 2017, financial buyers (both through stand-alone purchases and deals done by their portfolio companies) have announced 511 tech transactions, slightly ahead of the 506 deals announced by tech vendors on the Nasdaq and NYSE, according to 451 Research’s M&A KnowledgeBase. Even more telling is the current trajectory of the two groups. PE firms, which have increased the number of acquisitions every single year for the past half-decade, are on pace to smash the full-year record of 680 PE transactions announced last year. Meanwhile, US-listed acquirers are almost certain to see a second consecutive decline in M&A activity, with the full-year 2017 number tracking to almost 20% below the totals of 2014 and 2015.

The dramatic shift in the tech industry’s buyers of record has been brought about by changes in both acquiring groups. PE shops have never held more capital than they currently hold, which means they need to find markets where they can put that to work. (The tech industry, which is aging but still growing, offers bountiful shopping opportunities.) Cash-rich buyout firms, which are built to transact, have simply taken the playbook they have used on their shopping trips through other markets such as manufacturing and retail, among others, and applied it to the technology industry.

In contrast to the ever-increasing number of PE shops and their ever-increasing buying power, the number of tech companies on the Nasdaq and NYSE has been dropping for years. (Indeed, the overall number of US traded companies has been declining for years, with some estimates putting the current count of listings at just half the number it was 20 years ago.) For instance, some 38 tech vendors have already been erased from the two US stock exchanges so far in 2017, according to the M&A KnowledgeBase.

Yet even those companies that still trade on the exchanges aren’t doing deals at the same rate they once did. In years past, some of the big-cap buyers — the ones that used to set the tone in the tech M&A market — would announce a deal every month or so. Now, public companies have slowed their pace, and PE firms have simply sprinted around them in the market.

Consider this tally, drawn from the M&A KnowledgeBase, of activity last month by the two respective groups. On the lengthy list of tech giants that didn’t put up a single print at all in July: Oracle, Microsoft, IBM, Hewlett Packard Enterprise, Salesforce and SAP. Meanwhile, financial acquirers went on a shopping spree. H.I.G. Capital, Francisco Partners, Clearlake Capital and Thoma Bravo (among other PE shops) all inked at least two prints last month.