Contact: Brenon Daly

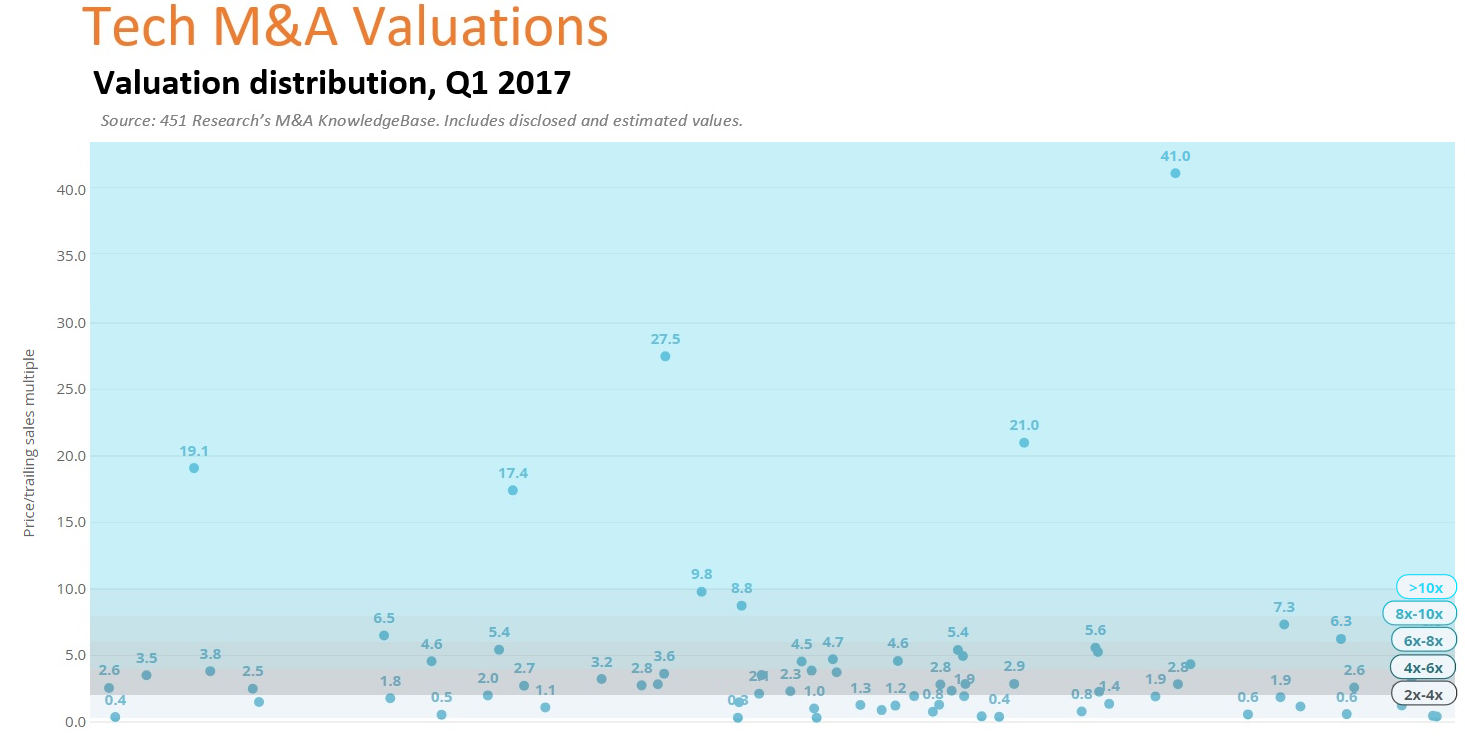

If spending on tech M&A was sporadic in the opening quarter of 2017, the valuations paid in those deals largely held to typical patterns. There were a handful of transactions sporting enviable double-digit multiples, along with a whole backlog of deals that printed in the low single digits. Between those bands, however, there was one range that generally features a host of transactions but has been relatively quiet so far this year: slightly above-market valuations.

Specifically, the January-March quarter recorded just three deals that valued target companies at 6-8x trailing sales, according to 451 Research’s M&A KnowledgeBase. That’s fewer than any quarter in 2016, and just slightly more than half the average number of similarly valued transactions each quarter last year. Given the generally lumpy nature of M&A, we obviously don’t want to make too much out of pricing trends in any single quarter. But it is important to note the falloff in activity because this valuation range often stands as a fairly accurate barometer for the health of the overall M&A market.

Yet this segment gets ignored, with more attention paid to splashy, headline-grabbing deals such as Cisco lavishing $3.7bn on AppDynamics, a company that barely cracked $200m in revenue last year. For a variety of reasons, however, we wouldn’t hold out this transaction as representative of the nearly 1,000 deals tallied last quarter in the M&A KnowledgeBase. (Cisco, which is trading at its highest level since the internet bubble, had to outbid Wall Street for AppDynamics, at a time when ‘dual tracking’ still isn’t much of a threat. As if to indicate that, indeed, those were rather singular influences on the deal, consider the fact that AppDynamics garnered the highest price for any VC-backed startup in three years.)

Instead, we would look below those one-off transactions. More relevant to most tech acquirers are deals where they have to stretch, but not contort, on pricing. These transactions – carrying, again, a 6-8x multiple and generally falling in the midmarket in terms of size – tend to serve more usefully as comparable deals for the corporate and financial acquirers that do the overwhelming majority of tech M&A. Here we’re talking about recent transactions such as Akamai reaching for SOASTA, or Hewlett Packard Enterprise further bulking up its storage portfolio with SimpliVity. Both of those deals fall into the 6-8x sales range (according to our understanding) and represent decidedly midmarket bets by big-name buyers. In other words, just the sort of transaction that’s vital to the broader tech M&A market, but generally gets overlooked – particularly so far this year.