Contact: Brenon Daly

We noted earlier this week that IT budgets are tightening, meaning growth could get harder to find as the year rolls along. Sluggish expansion and diminished outlooks have already hit some of the tech industry’s major names. And while they search uncertainly for a way to bump up their top lines, they aren’t necessarily looking to M&A. We’ve already seen a few key companies, particularly those accustomed to growing at a rapid clip, step out of the market.

- Apple is shrinking after a decade and a half of uninterrupted growth that was the envy of the tech industry. In the previous three years, when it was growing revenue at an average of a mid-teens rate, the company printed about an acquisition every month, according to 451 Research’s M&A KnowledgeBase. Yet it hasn’t been nearly that active as revenue declined. Earlier this week, Apple bought an early-stage analytics provider – its first deal since January.

- Former highflier FireEye has dramatically come back to earth. The security specialist now expects to earn just $100m in additional revenue in 2016, which is half the $200m in new revenue it posted in 2015. That means FireEye would generate mid-teens growth this year, just one-third the level it grew last year. FireEye hasn’t announced a deal in the past six months.

- Like FireEye, Twitter is growing at only one-third the rate it was last year. (In its second quarter, Twitter increased revenue just 20%, compared with 61% in Q2 2015.) According to the M&A KnowledgeBase, Twitter has done 19 acquisitions since its IPO in November 2013. However, just one of those transactions has come in the past year, as the company has struggled with attracting new users and selling more ads to that decelerating audience.

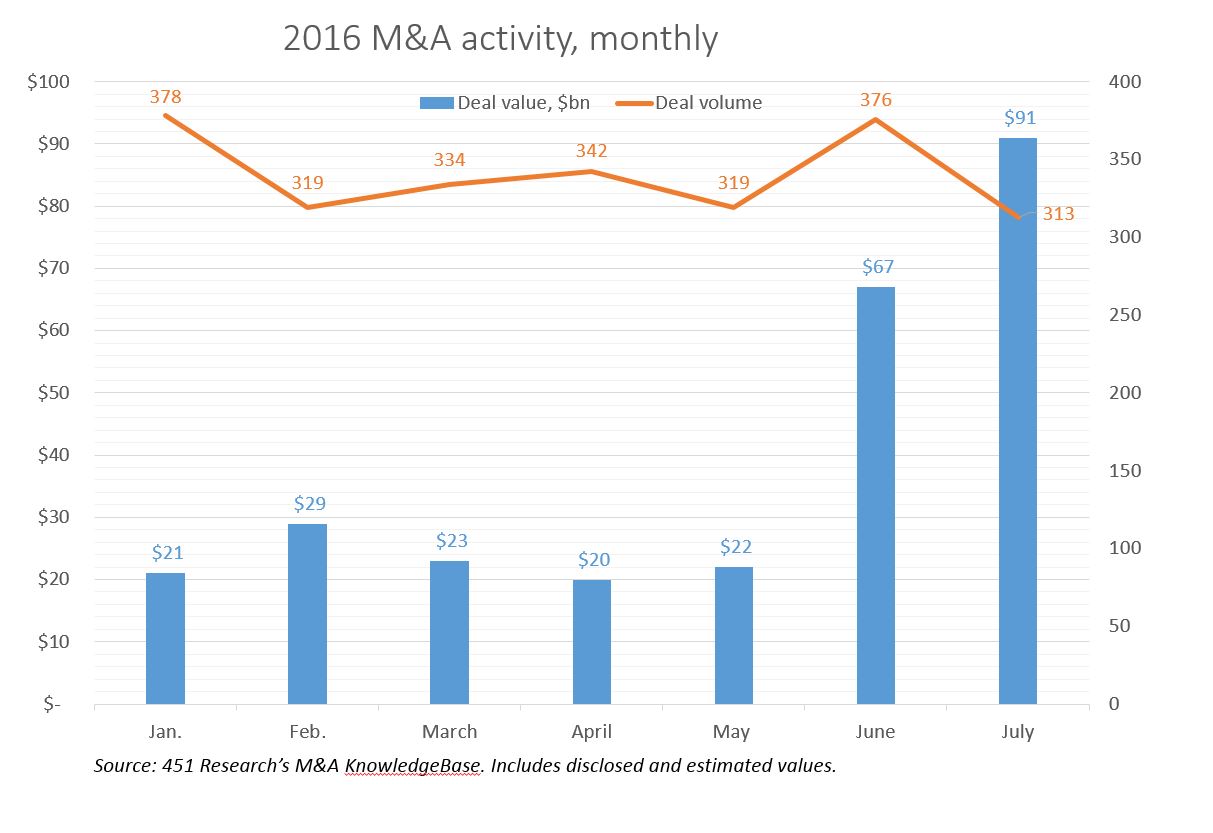

As marquee tech firms find their growth slowing or even reversing, they are more likely to hunker down. The first order of business for a company that’s stumbling is to understand where it tripped up and what it needs to do to regain its stride. (As they say, growth masks a lot of problems.) Acquisitions – potentially expensive and often irrecoverably distracting – don’t really fit strategically when a vendor is doing layoffs (FireEye) or looking to sublease some of its headquarters (Twitter). If more of the tech industry does indeed feel the pinch of tightening IT budgets, the recent surge in M&A could slow substantially for the rest of the year.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.