Contact: Brenon Daly

Michael Dell has had his say. Same with Joe Tucci. But are the customers of the Dell and EMC chief executives actually buying what the two companies are saying about the tech industry’s largest acquisition? Only one way to find out: ask them.

With the ink barely dry on the announcement of Dell’s record-breaking $63.1bn purchase of EMC, 451 Research’s Voice of the Enterprise surveyed almost 450 IT decision-makers to get their sense of what they liked about the transaction, what worried them and, most importantly, how the proposed combination would affect their IT spending. (See the executive summary of the survey results.)

Ultimately, the sentiment and intention voiced by customers – such as those we surveyed – will determine whether Dell-EMC builds itself into a true IT infrastructure and services powerhouse or, like so many other multibillion-dollar tech pairings, devolves into an unhappy, underperforming union. So what does the ‘buyside’ think about the deal?

- Overall, three out of 10 respondents gave the mega-transaction a thumbs-up, compared with two out of 10 who voted it down. However, within that broad assessment, there was a clear division between the Dell and EMC camps. Dell-only customers (those that currently buy no products from EMC but do buy from Dell) were almost three times more likely to have a favorable view of the deal than EMC-only customers (40% vs. 15%).

- Why are a plurality of EMC customers bearish about the company’s prospects inside Dell? For the most part, they still view Dell as dealing in commodity technology. More than four out of 10 EMC-only customers consider Dell primarily a PC supplier, and another 20% identify it as mainly a low-cost IT supplier.

As we look at the results of the survey, particularly the perception of Dell as a ‘box maker,’ we can’t help but think that some of the sharp divergence between the views of the two customer bases is attributable to the sharp divergence between the M&A programs at the two companies. To be blunt, Dell was late to the game, with a long-held institutional preference for organic development rather than inorganic expansion. In contrast, EMC liked to shop, spending more than $20bn on 100+ acquisitions over the past 15 years, according to 451 Research’s M&A KnowledgeBase.

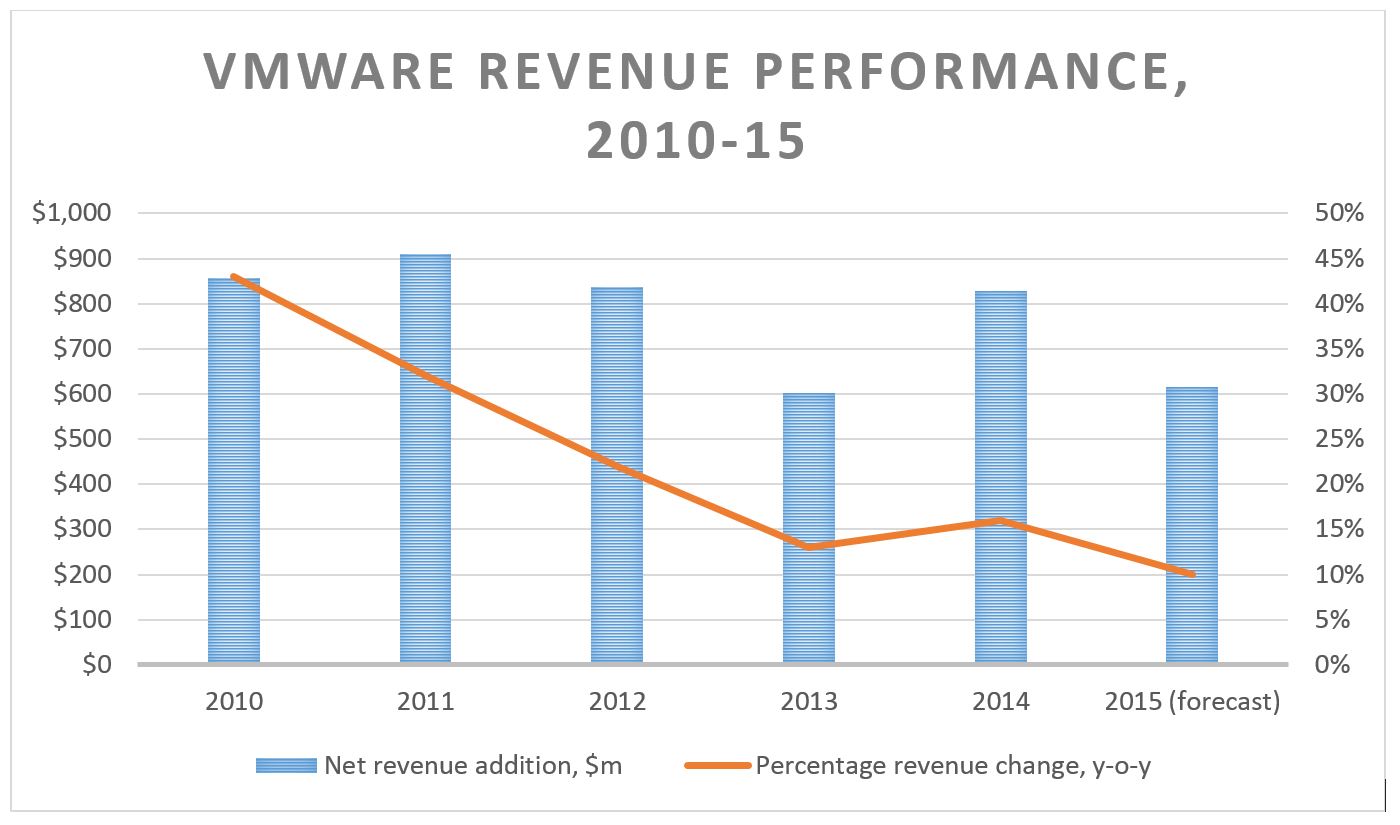

In fact, by the time Dell (belatedly) got its M&A machine revving in mid-2007, EMC had already purchased many of the key components of its ‘federation’ business: Documentum, RSA and, of course, the crown jewel of VMware. One existential question – which, for the record, we didn’t ask our panel of IT buyers – was whether Dell would have even needed to buy EMC outright if it had picked up some of the other companies that were nabbed by EMC. Again, to see the responses to questions we did ask on the Dell-EMC combination, check out the executive summary.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA .