As customer experience (CX) continues to spur digital transformation projects, Wipro makes another reach in that category with the acquisition of Rational Interaction, a CX and marketing consulting shop. The deal comes as the surging pace of digital transformation projects is propelling the convergence of disparate services markets and remaking the IT services landscape.

The purchase of Seattle-based Rational and its 300 employees marks Wipro’s third acquisition of a CX consulting business, according to 451 Research‘s M&A KnowledgeBase. With the deal, Wipro is aiming to expand its market share of digital transformation projects – a growing market that it set out to capture three years ago with the launch of Wipro Digital, which now accounts for more than one-third of its revenue.

Wipro is not alone in expanding its capabilities to move into digital transformation as vendors continue to roll out those expansive modernization strategies. According to 451 Research’s Voice of the Enterprise: Digital Pulse, Workloads & Key Projects report, 70% of all organizations were either executing or developing a digital transformation strategy. As such, many of Wipro’s peers in IT services, management consulting, and advertising and marketing services have aimed to extend their ability to service expansive digital enterprise projects, rather than stand-alone IT, marketing, management or operations engagements.

Accenture, for example, put up 26 prints in 2019, making it the most active tech buyer last year as it expanded its digital chops in web design, software development, data analysis, brand development and infosec, among other areas. Ad-agency holding companies Interpublic and Publicis inked 10-figure pickups of Acxiom and Epsilon, respectively, to position themselves as data management experts. And four of the six deals done by Wipro’s regional rival, Tech Mahindra, last year brought on CX expertise.

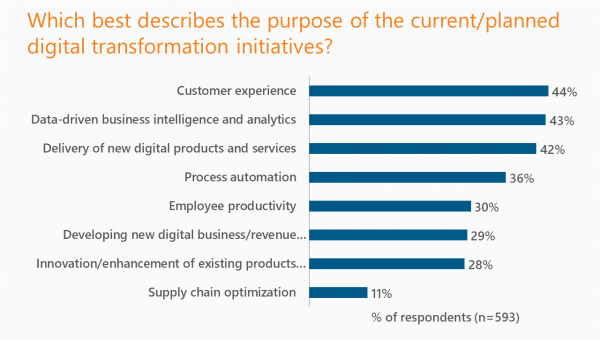

Rational Interactive’s peers, with expertise in marketing, design and other customer experience capabilities, are likely to continue to be in demand as CX often spurs enterprise-wide digital projects. In the above-mentioned survey, 44% told us that ‘customer experience’ is the primary purpose behind their digital transformation initiative. And that’s bolstering the valuations of vendors with the relevant expertise. Our data shows that service providers in marketing and web design commanded a median 2x trailing revenue in acquisitions last year, almost a full turn higher than the median multiple across the broader IT services and outsourcer categories.

Figure 1: Purpose of digital transformation