by Brenon Daly

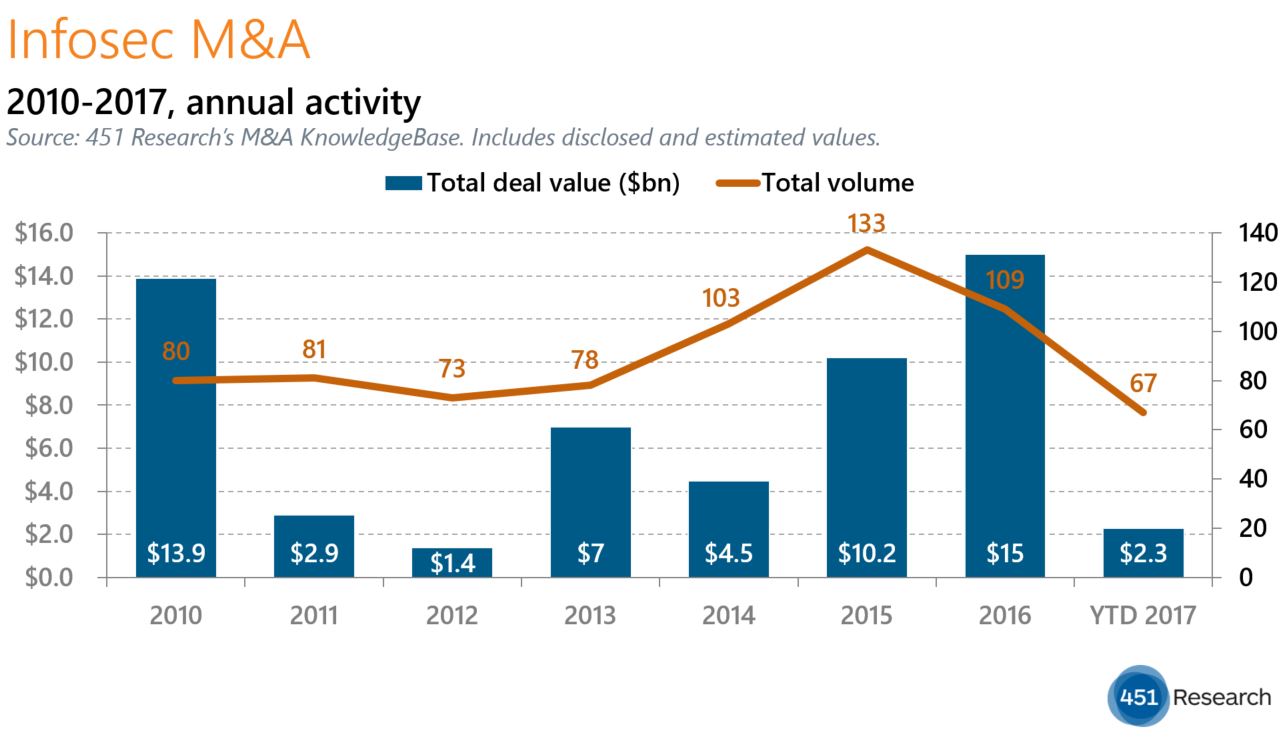

Playing defense can be a lucrative strategy. Along with the record deal volume in the information security (infosec) market this year, valuations across the fast-growing sector have surged to their highest level. Already in 2018, 451 Research’s M&A KnowledgeBase lists eight transactions that have gone off at price-to-sales multiples of more than 10x, based on disclosed or estimated terms.

These double-digit valuations have helped to push the multiple across the entire infosec market to new heights, twice as rich as virtually all other major IT sectors. According to the M&A KnowledgeBase, acquirers have been paying 8.1x trailing sales for the infosec companies they have picked up so far this year.

For comparison, the next-richest segment (infrastructure software) checks in at 6.6x trailing sales. One sign of how inflated that market has become is the surprisingly rich valuation of infrastructure software titan CA Technologies. Broadcom is paying the highest price for CA shares since the internet bubble collapsed. The deal values CA at 4.5x sales, roughly a turn higher than other large software vendors that aren’t really growing. Additionally, Salesforce paid more than 20x trailing sales for MuleSoft in March.

More broadly, valuations in the 10 other IT sectors we track in the M&A KnowledgeBase are all less than half the median valuation in infosec. For instance, application software transactions this year are going off at 3.4x trailing sales, which is roughly consistent with the two previous years.

Of course, as in any small market, a few richly valued deals can skew the overall valuation for the sector. (The number of infosec prints each year is only about one-tenth the number of application software transactions in any given year.) And the infosec market has seen an unusually large number of big prices paid for very early-stage startups. Deals such as Palo Alto Networks-Evident.io and Splunk-Phantom Cyber are certainly pushing the median multiple higher. But even outside those outliers, acquirers are having to reach deeper than ever before to secure the security providers they want to buy.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.