Contact: Brenon Daly

Sure, the number of deals and spending on them in 2015 blew away anything we’ve seen since we were surfing the Web on Netscape browsers, but there was a whole lot more going on inside last year’s activity. 451 Research subscribers can get our full report on what happened last year and what’s likely to play out this year. Looking inside the record deal flow we recorded in 451 Research’s M&A KnowledgeBase, for instance, we saw a number of highlights from 2015:

- Acquirers have never announced more tech, media and telecom (TMT) transactions valued in the billions of dollars than they did in 2015, including two of the three largest pure tech transactions in history.

- Last year saw an unexpectedly large number of tech giants either sit out the record M&A activity altogether (Symantec, the former JDS Uniphase) or significantly dial back their acquisition programs (SAP, Oracle, Yahoo, Intuit).

- The value of divestitures by US-listed tech companies hit a new record, coming in at twice the average annual amount over the past half-decade.

- Private equity firms announced the most acquisitions ever for the industry, more than doubling the number of deals they did during the recent recession.

- Even as interest rates ticked higher, buyout shops paid unprecedentedly rich multiples at the top end of the market in their purchases.

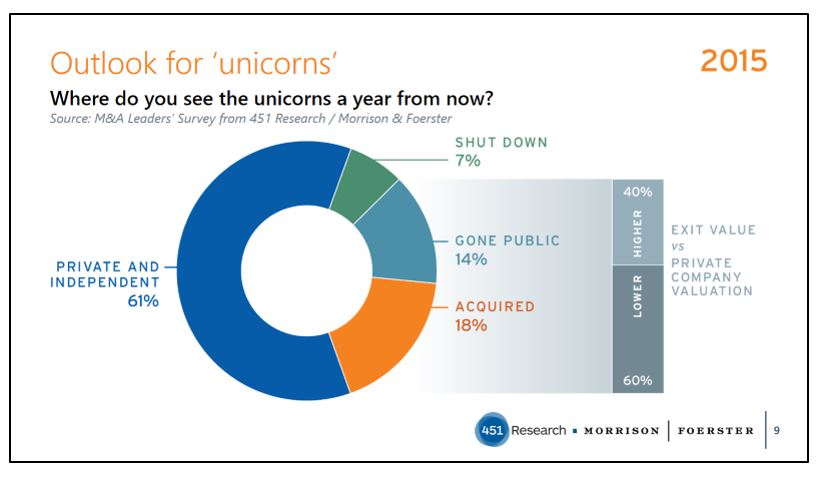

- Despite the record number of startups valued at $1bn or more, just one VC-backed company recorded a 10-digit exit in 2015, down from an average of four exits each year over the previous three years.

Our report not only highlights these trends, but also maps them to the views from the main participants in the tech M&A community to give a sense of what will shape acquisitions in the coming year. See the full report.

Valuations of significant* tech transactions

|

Source: The 451 M&A KnowledgeBase *Average multiple in 50 largest acquisitions, by equity value, in each year.

For more real-time information on tech M&A, follow us on Twitter @451TechMnA