Contact: Brenon Daly

When big acquirers step out of a market, they can leave behind a big hole. In the case of the current tech M&A market, it’s a multibillion-dollar hole. We noted in our full report on the just-closed second quarter that the value of tech and telecom acquisitions dropped 30% from Q1 to Q2, hitting a four-year low for quarterly spending of just $55bn in the April-June period, according to 451 Research’s M&A KnowledgeBase. The main reason for the recent slump in spending is the disappearance of many of the tech industry’s biggest buyers.

At the start of this year, many well-known acquirers — the ones that often serve as bellwethers for the tech industry — were actively inking significant deals. Intel, Cisco and Hewlett Packard Enterprise all announced acquisitions valued at more than $1bn in Q1. Since then, however, most of the busiest tech giants have shifted their M&A machines into neutral. In their place, two groups of buyers have emerged: old-line telcos and private equity (PE) firms.

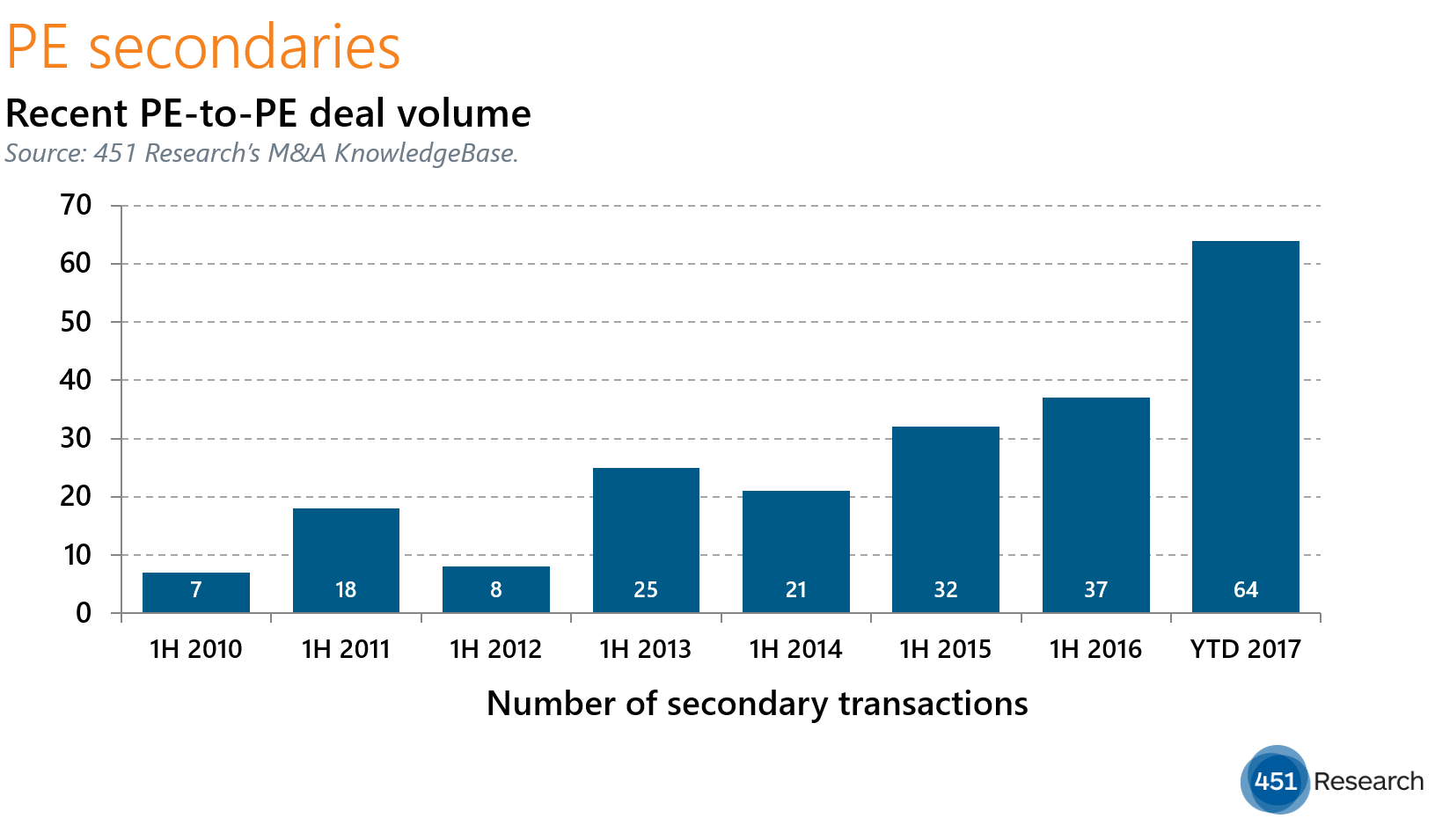

Yet these newly assertive acquirers haven’t come close to closing the gap, in terms of M&A spending, left by the missing corporate shoppers. (That’s not for lack of effort among the financial buyers. PE firms announced a record level of tech transactions in Q2, eclipsing the number of deals done by US-listed corporate acquirers for the first time in history, according to the M&A KnowledgeBase. Our Q2 report has more details on activity and forecasts for the buyout shops.)

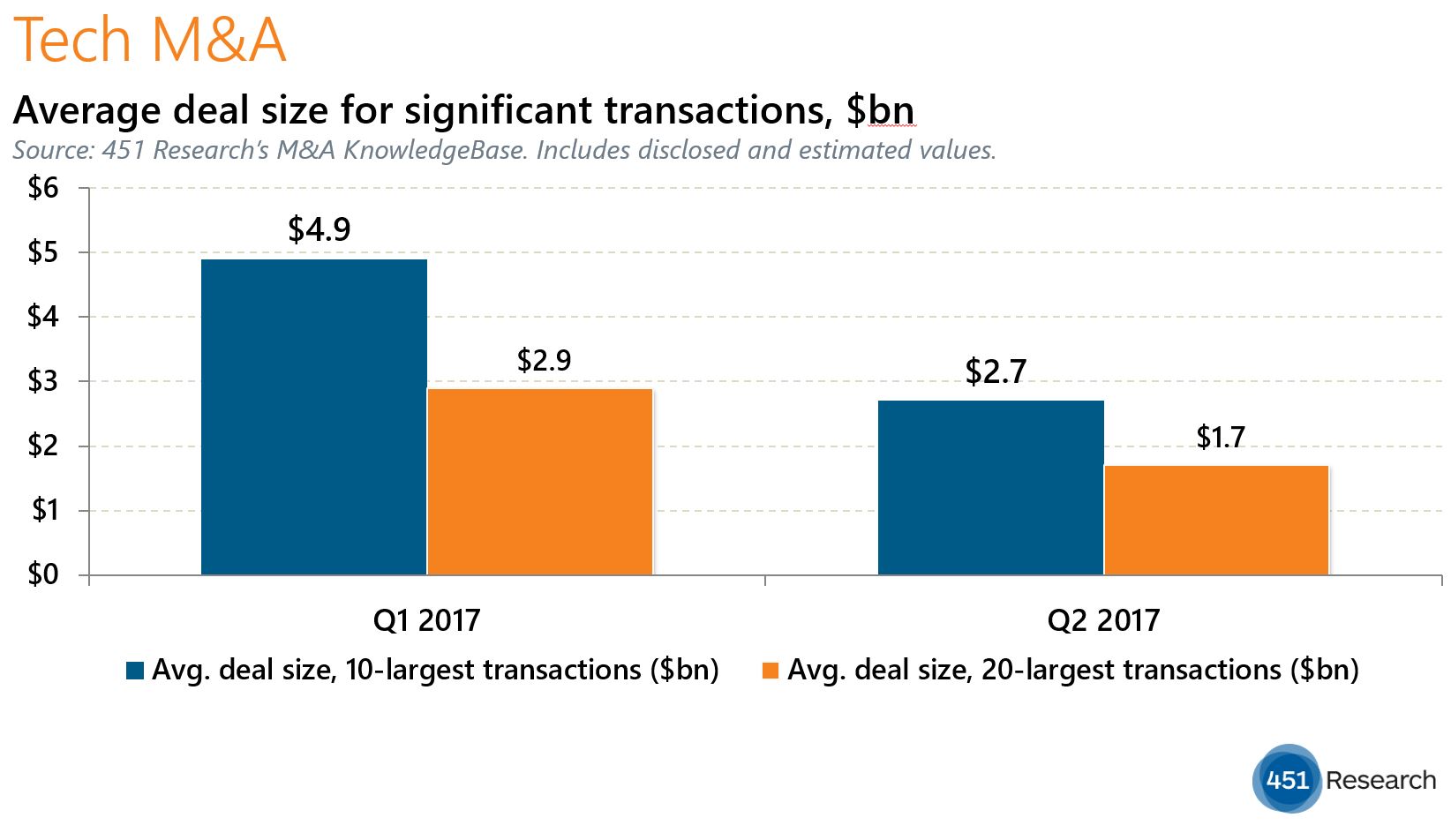

As one indication of what went missing when big-name corporate acquirers took an early summer hiatus from big-dollar deals, consider this: Only one of the five largest transactions announced in the first half of 2017 printed in Q2. That shift in strategy and spending by corporate buyers dramatically crimped deal flow at the top end of the tech M&A market. According to the M&A KnowledgeBase, the average value of the 20 largest tech transactions announced in the first three months of 2017 stood at $2.9bn. That’s 70% higher than the average of $1.7bn for the 20 largest deals announced in the just-completed Q2.