Contact: Brenon Daly

The quintessential Silicon Valley deal is drying up. Sales of VC-backed tech startups, which once provided a steady flow of money to entrepreneurs and their backers, are down sharply so far this year, compared with recent years. And while the impact of the narrowing of that exit will be primarily felt along Sand Hill Road, the cause of the slump traces back to Wall Street.

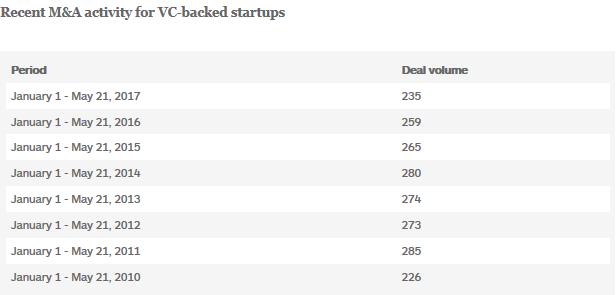

So far this year, just 235 VC-backed tech companies have sold, according to 451 Research’s M&A KnowledgeBase. That paltry level represents the fewest startups sold in the first five and a half months of any year since 2010, even as the overall tech M&A market has broadened and increased the current number of total tech transactions by nearly 15% since the start of the current decade. Year to date, M&A volume for VC-backed vendors is running 13% lower than the average number of deals over the past five years, according to the M&A KnowledgeBase.

The sharp decline in exits comes as the ranks of the startups are swelling, with thousands of businesses receiving venture investment each year. So if the slowdown isn’t coming from the supply side, that leaves only the demand side. And indeed, we can narrow the cause of the recent slump to one particular set of startup buyers: US public companies.

For the first half of the current decade, according to the M&A KnowledgeBase, NYSE- and Nasdaq-listed vendors accounted for more than 40% of the purchases of VC-backed companies. In some years, that approached nearly half of the transactions. So far this year, the tech industry’s big fish have gobbled up the minnows in only slightly more than one-third of the deals. If the classic startup-sells-to-tech-giant transaction isn’t playing out as often as it once did, that’s primarily because many of the tech industry’s one-time biggest buyers have themselves been bought.

Some behemoths have been consolidated by fellow behemoths, with the net effect that the combined entity – perhaps still struggling with integrating a business that does hundreds of millions of dollars, or even billions of dollars, of revenue – doesn’t have the capacity to do anywhere near as many deals as the two stand-alone companies did. Consider the relative M&A rates for Dell and EMC on both sides of that blockbuster pairing. In other cases, tech giants have gone private, with buyout shops that tend to focus on financially optimizing existing businesses, rather than trying to bump up revenue growth through potentially costly acquisitions of shiny new startups. For instance, BMC has done only three purchases since its leveraged buyout four years ago, down from an average of four acquisitions in each of the three years leading up to its take-private.

Source: 451 Research’s M&A KnowledgeBase

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.