by Brenon Daly

The retail industry is learning the costly lesson that clicking an online shopping cart button has relatively little in common with pushing a shopping cart down a store aisle. The deals that retailers have struck to bridge the physical and digital worlds just haven’t been ringing the cash registers. The latest example: Nordstrom wrote off more than half of its $350m acquisition of Trunk Club.

It wasn’t supposed to be this way. The ‘bricks and clicks’ pairings made sense, at least in the pitchbook. Retailers needed to be more represented in places where their customers were actually shopping. (The National Retail Federation recently forecast that a record 56% of shoppers plan to buy online this upcoming holiday season, tying for the top spot among all customer destinations.)

In addition to the need to go digital, buyers were also lulled into a false sense of confidence by oversimplifying the fundamental premise of these proposed deals: Acquire a complementary Web-based storefront, with all of the accompanying technology and talent, and then just slap that in front of the massive back end that the big retailer has already built.

These theoretical transactions seemed a perfect fit, taking care of the specific challenges each vendor felt in its particular model. For the e-tailer, creating supply chains and delivery centers would likely cost tens if not hundreds of millions of dollars of capital expenditure, which is rarely a high-returning use of risk capital such as VC. (Not to mention those venture dollars, in general, are getting harder to pull in.) For retailers, they would get the digital smarts around marketing and selling on the Web, without having to painstakingly repurpose existing resources or slowly hire scarce digital talent.

And yet, that has turned out to be a spurious strategy. Online retailing isn’t any more of an extension of traditional retailing than online media is an extension of traditional media. With Nordstrom’s tacit admission that its M&A push into the ether hasn’t generated the expected returns, we wonder about a significantly larger bet – roughly 10 times the size of Nordstrom’s purchase of Trunk Club – that Wal-Mart has placed on Jet.com.

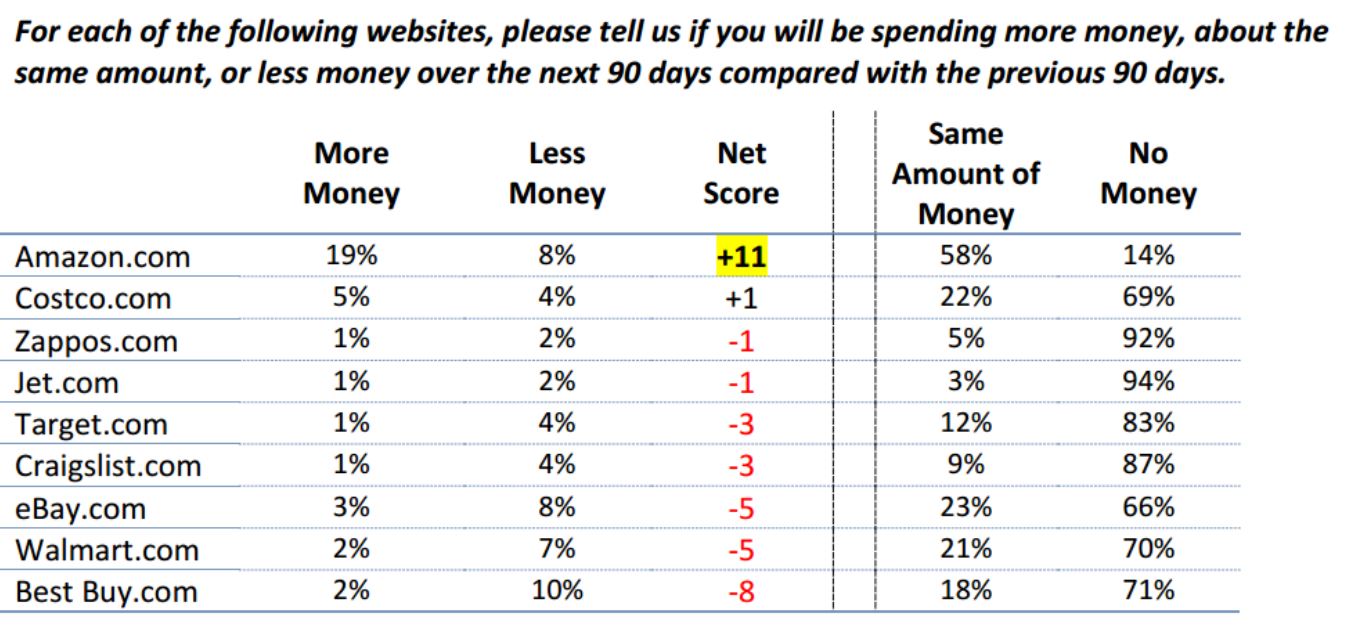

The retailing giant’s pickup of Jet.com last August stands as the largest e-commerce transaction of the past 15 years and the biggest sale of a VC-backed startup in two and a half years. However, the early returns on that blockbuster pairing don’t appear promising. In a survey by 451 Research’s Voice of the Connected User Landscape in mid-September, just after Wal-Mart closed the deal, more people projected they’d be spending less at Jet.com than spending more at the website through the end of the year.

Source: 451 Research’s Voice of the Connected User Landscape

Source: 451 Research’s Voice of the Connected User Landscape

For more real-time information on tech M&A, follow us on Twitter @451TechMnA.