Contact: Brenon Daly

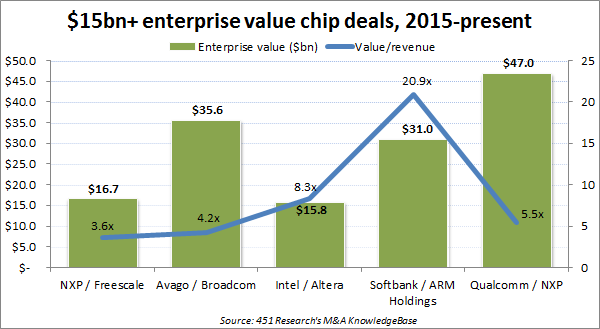

This year is proving to be a very rich vintage for tech M&A. At the top end of the market, acquirers are paying higher multiples than they’ve paid in any year since the end of the recession. Consider the rather mature semiconductor industry, where, historically, acquisition activity has been characterized by low-multiple consolidation. That hasn’t been the case so far in 2016, where chip deals have accounted for three of the four largest transactions. Rather than dragging down the broad-market valuation, they are actually boosting it substantially.

The chip industry’s platinum valuation was once again on display in Qualcomm’s $39.2bn purchase of NXP, the latest – and largest – blockbuster transaction in the semiconductor industry. In addition to Qualcomm-NXP, there have been two other semiconductor deals valued at more than $10bn. The average multiple in those big-ticket transactions stands at an astounding 11.9x trailing sales. That’s more than twice the average multiple of 5.4x trailing sales for the three chip deals valued at more than $10bn last year, according to 451 Research’s M&A KnowledgeBase.

And while chip companies have been spending freely, other big buyers are also paying up. Microsoft’s $26.2bn play for LinkedIn values the online professional network at more than 8x trailing sales. Oracle, which itself trades at a little more than 4x trailing sales, has offered to buy NetSuite in a transaction that values the SaaS vendor at more than 10x trailing sales. (Although it’s not certain that the deal will actually go through due to disgruntled shareholders.)

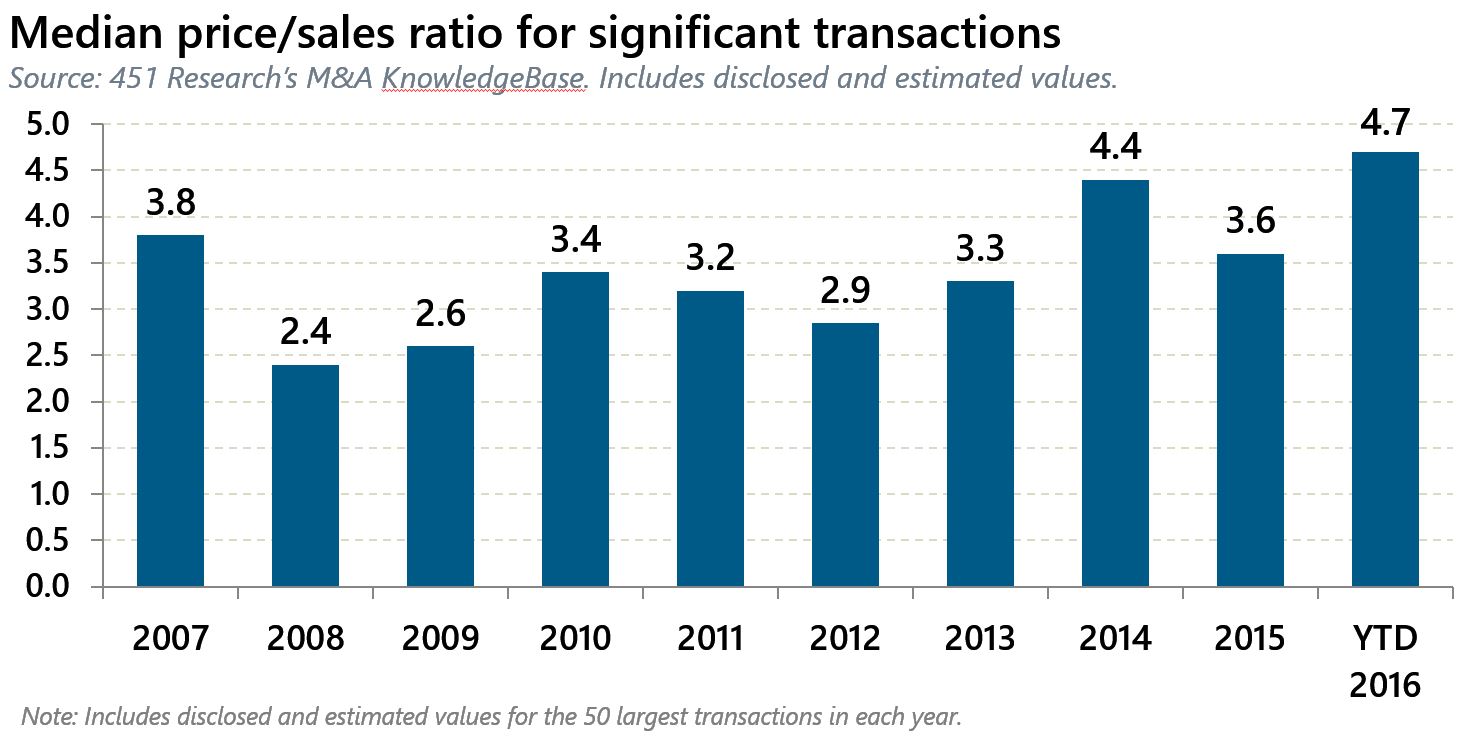

More than any other recent year, the driver for those large-scale transactions in 2016 has been growth, whether it’s innovating existing products through M&A (Microsoft-LinkedIn), obtaining a presence in the nascent but expanding market of mobility and the Internet of Things (semiconductor deals), or acquiring a faster-growing delivery model for software (Oracle-NetSuite). Overall, the 50-largest tech acquisitions so far this year have gone off at 4.7x trailing sales, according to the M&A KnowledgeBase. That’s the highest level since the recent recession and a full turn higher than the 3.6x trailing sales recorded in 2015.