Contact: Brenon Daly

Regardless of the outcome of tonight’s inaugural US presidential debate, this year’s election process has already turned off voters. The prospect of casting a ballot for either of the two mainstream presidential candidates – who are both currently viewed ‘unfavorably’ by a majority of US voters – in an increasingly rancorous campaign is casting a cloud that expands far beyond Washington DC. The electoral disenchantment is also likely to hurt business.

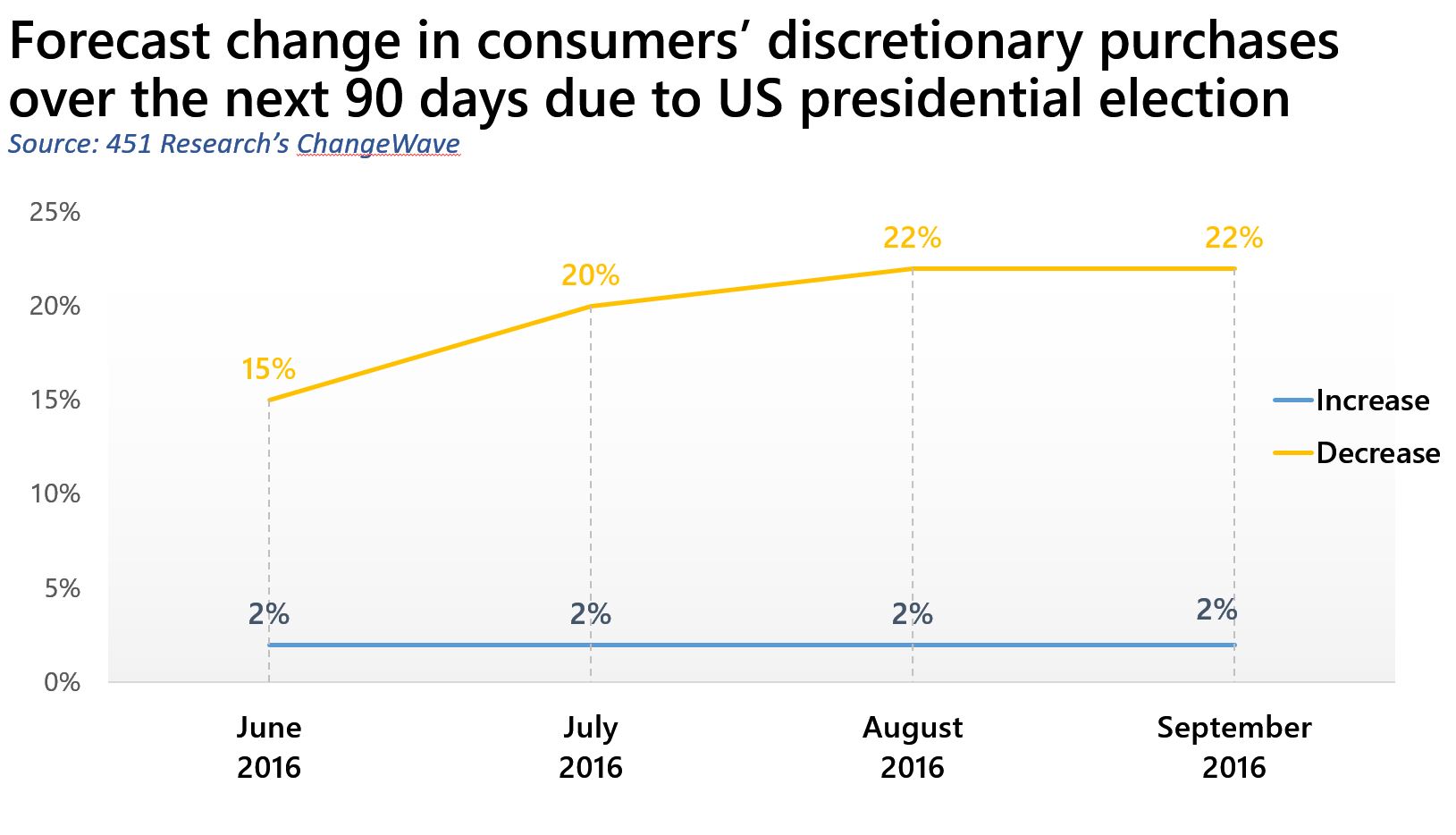

That’s one conclusion of a new survey from 451 Research’s ChangeWave service, which last week asked more than 1,900 consumers what impact the ongoing US presidential election will have on their shopping plans for the next three months. The vast majority of respondents (71%) said the Trump vs. Clinton circus would have no impact on their discretionary spending through the end of the year. However, if we look at the minority-but-still-sizable remaining portion (29%), those respondents overwhelmingly indicated they are putting away their checkbooks. In fact, the number of consumers who forecast they would be decreasing their discretionary purchases (22%) was 11 times higher than those who said they would be increasing their purchases (2%).

We mention the ChangeWave finding because it may (and here we emphasize the word ‘may’) help explain some of the slowdown in recent tech M&A activity. Obviously, some qualifications are needed any time we extrapolate results from a consumer-based survey to the corporate world. To be clear, ChangeWave polled consumers only about their plans for individual discretionary purchases, and did not specifically address corporate M&A. Nor did it focus on tech. However, given that companies are just a collection of people who tend to bring their perceptions with them to the office, and acquisitions can sometimes be viewed as a discretionary purchase, we would make the case that ChangeWave’s finding has relevance to the tech M&A community.

Regardless of whether the presidential election is actually knocking deals off the table, something is slowing down activity. In the first half of 2016, tech acquirers announced an average of 350 transactions each month, according to 451 Research’s M&A KnowledgeBase. Both July and August came in below that level. In fact, last month’s total of just 297 tech deals, representing a 14% decline from the monthly average in the first half of 2016, was the first time since March 2014 that M&A volume failed to top 300. And while September won’t wrap up until the end of this week, this month is tracking even weaker than last month. (We are on pace for about 270 announced transactions for September.) In other words, as we get closer to election day, M&A activity is dropping off.