by Brenon Daly

So much for the comeback of the tech IPO market. Although SecureWorks did manage to make it public on Friday, the managed security service provider – along with its 17 underwriting banks – had to trim both the size and price of its offering to get investors interested. In afternoon trading on the Nasdaq exchange, SecureWorks shares were changing hands around its offer price of $14, which is lower than the range it laid out earlier.

Recent enterprise tech IPOs*

|

*Includes Nasdaq and NYSE listings only

SecureWorks’ underwhelming debut comes as the first enterprise tech offering since Atlassian hit the market in December. In the intervening months, concerns about slowing economic growth have swept through the world’s equity markets. Here in the US, the Nasdaq Composite Index dropped 15% in the first six weeks of this year. During that bear market, tech companies prudently opted not to continue with their offerings, much as a ship captain would not choose to set sail in stormy seas.

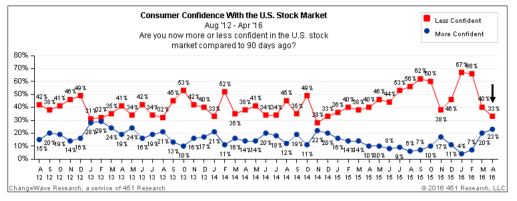

However, by late April, as SecureWorks launched its delayed offering, the storm had mostly passed. The Nasdaq has recovered its losses from earlier in the year, and Wall Street was no longer shaky ground. An April survey of individual investors by ChangeWave (a subsidiary of 451 Research) showed a dramatic turnaround in sentiment: Only one-third of respondents to our April survey said they were ‘less confident’ in the stock market than they were three months ago. That was just half the level at the start of 2016, and the lowest reading in more than a year. On the other hand, almost one-quarter of the respondents indicated they are feeling ‘more confident’ in Wall Street, which was the most-bullish reading we’ve had in three years.

So SecureWorks wasn’t necessarily heading out into stormy weather. Yet it still had to give up a fair amount to get public, which doesn’t seem to make much sense. (And Wall Street is nothing if not rational and judicious.) Sure, the company is unprofitable. But red ink has never stopped investors from buying, even when a company counts its revenue in the tens of millions of dollars but its net losses in the hundreds of millions of dollars. (For the record, SecureWorks is nowhere near that level, having lost $72m on revenue of $340m in its most-recent fiscal year, which ended in January.)

If SecureWorks’ so-so IPO wasn’t entirely due to the broad market or the company, maybe it had something to do with the offering itself. The basics of the SecureWorks IPO could be summarized like this: An established tech company acquires a fast-growing startup, then spins off a minority stake of a class of equity that effectively gives shareholders no voice in the direction or outcome at the company. That’s virtually the same structure as the VMware IPO, which hasn’t necessarily been kind to the company’s minority shareholders.

![Alibaba_active_buyers_copy[1]](../../files/2016/04/Alibaba_active_buyers_copy1.png)