Contact: Mark Fontecchio

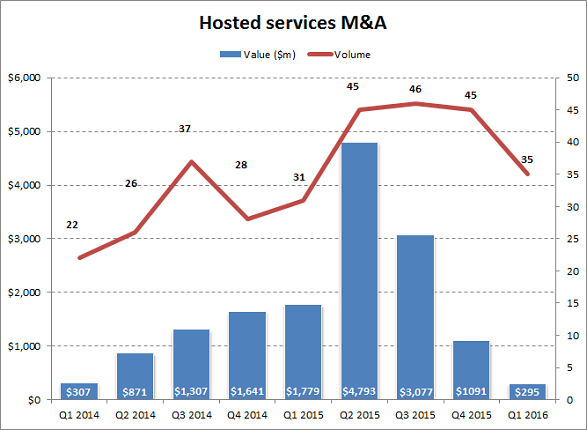

The value of hosted services M&A crashed to Earth in Q1, despite an uptick in deal volume. Following a boom of six consecutive quarters with more than $1bn in deal value, last quarter saw less than $300m in transactions, the lowest total in four years. The downward movement in hosted services reflects the broader tech M&A sector, which saw a slowdown as credit markets tightened and stocks gained volatility. In addition to that, there just aren’t many large-scale pairings left to be had. The US hosting market underwent a strong period of consolidation over the past few years, and Europe’s not far behind it.

Asset acquisitions, such as one-time datacenter deals, accounted for one-third of the activity in hosted services in the quarter as large providers made modest purchases to meet demand and enter new markets. Regional expansion transactions included serial acquirer Carter Validus buying two facilities in Georgia and Texas, and Zayo Group scooping up a 36,000-operational-square-foot datacenter in Dallas. These acquisitions fit one of the three major trends we anticipated for hosted services M&A in 2016: that datacenter operators would continue to grow regionally through M&A. To boot, the biggest hosted services transaction was the $130m leaseback agreement between CyrusOne and CME Group for an 80,000-operational-square-foot facility in Aurora, Illinois.

Meanwhile, service providers didn’t spend much to move up the value chain into managed services and similar segments. Instead, they opted to stay within their wheelhouse – nearly 43% of hosted services deals last quarter were colocation acquisitions, nearly double the portion from a year earlier. We expect those types of transactions to pick up the rest of the year alongside continued geographic datacenter consolidation. Overall hosted services M&A will also likely accelerate, as the first quarter is historically the year’s slowest in both volume and value.