by Brenon Daly

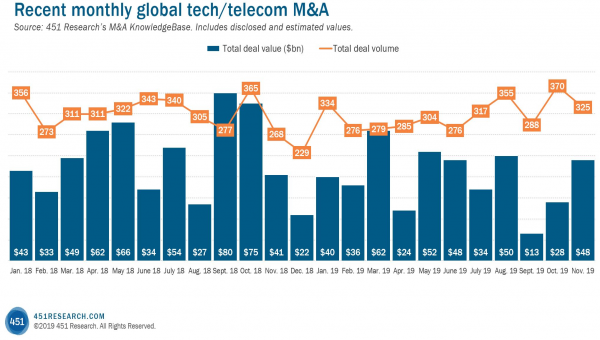

Tech M&A spending rebounded in November after two decidedly weak months. Last month’s pickup put this year back on track to record slightly less than a half-trillion dollars’ worth of tech and telecom transactions for full-year 2019. However, that strength assumes the buying can broaden in the final month of what’s proving to be a softening period for recent tech dealmaking.

Across the globe, acquirers handed out $48bn in the just-closed month on tech deals, according to 451 Research‘s M&A KnowledgeBase. Our data indicates the value of transactions announced in November topped the combined total from both September and October. Yet, in one indication of the concentration of M&A activity in November, we would note that the M&A KnowledgeBase actually lists fewer $1bn+ prints in November than October, even as overall spending surged 70%, month over month.

More than half of November’s spending came in a single deal: Charles Schwab‘s $26.2bn purchase of rival TD Ameritrade. (The blockbuster consolidation meets our definition as a ‘tech’ transaction, albeit clearly as a fin-tech deal.) After that, however, both the number and – more significantly – valuation of acquisitions last month dropped off sharply.

In the second-largest tech transaction in November, buyout shop Apollo Global Management took Tech Data private for a pittance of its revenue. Granted, IT distributors like Tech Data operate on low margins with little protection for their business model. But even with that disclaimer, it’s striking that a company generating more than $35bn in sales fetched a terminal value of just $5.6bn. Similarly, Alphabet paid just 1.2x trailing sales for Fitbit in last month’s fifth-largest deal.

It wasn’t all cleanouts and closeouts, however. Lightly funded e-commerce browser plug-in Honey got a $4bn payday from PayPal, the kind of exit that keeps the VC dream alive. But far more often in November, deals got done at a mid- to low-single-digit multiple. In fact, the M&A KnowledgeBase shows November transactions going off at a median of just 1.8x trailing sales, a full turn lower than the average for deals announced from January to October.

With 11 months now in the books, tech acquirers have been averaging about $40bn in monthly M&A spending. (That’s down from an average of nearly $50bn per month in last year’s record run.) That decline can be traced back to buyers, particularly financial acquirers, stepping out of the market just since summer.

Our data shows the value of tech transactions in the back half of 2019 is on pace to be roughly 25% lower than the first half of the year. As we look ahead to the final weeks of the year, we expect a continuation of the trend of soft landings in the market – with fewer big-ticket deals and lower overall valuations – that we’ve seen recently. For tech M&A, this year will be a clear drop from last year.