by Brenon Daly

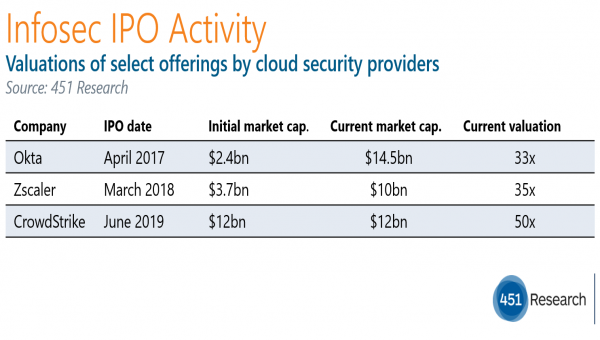

Other recent high-flying debutants in the information security (infosec) market have had to take some time to grow into their multi-unicorn status on Wall Street. Not so for CrowdStrike. The endpoint security vendor smashed all pricing expectations on its way to creating a stunning $12bn of initial market value in its IPO.

To put that number into perspective, CrowdStrike’s valuation is roughly equivalent to the M&A spending across the entire infosec market for any given year, according to 451 Research’s M&A KnowledgeBase. Or, sticking to comparisons in the IPO market, CrowdStrike’s debut market cap is twice the initial value created in IPOs by two other recent fast-growing cloud security startups:

Okta came public in April 2017 at a valuation of $2.4bn, and now commands a $14.5bn market cap.

Zscaler came public in March 2018 at a valuation of $3.7bn, and now commands a $10bn market cap.

In its most recent fiscal year, CrowdStrike posted revenue of $250m. Revenue more than doubled last year, helped in part by an astonishingly high dollar-based retention rate of roughly 140%. Although not yet profitable, the company showed some leverage in its model by holding its net loss at the same level over the past two years, even as it doubled revenue.

In the IPO, Wall Street is valuing CrowdStrike at nearly 50 times trailing sales. That’s a heady multiple, significantly eclipsing the current mid-30x price-to-sales multiples for both Okta and Zscaler.

CrowdStrike is, however, still looking up at the current trading multiple of Zoom Video Communications. Zoom shares have tacked on roughly 50% since debuting in April, giving the profitable and fast-growing videoconferencing startup a price-to-sales multiple of nearly 70x. If CrowdStrike could replicate Zoom’s trading in the aftermarket, the infosec startup would be tracking to nearly the same astronomical trading multiple later this summer.